BMAN21020 FINANCIAL REPORTING AND ACCOUNTABILITY 2021

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

BMAN21020

FINANCIAL REPORTING AND ACCOUNTABILITY

2021

![]()

Answer ALL questions

SECTION A (COMPULSORY)

1. Consolidated Financial Statements

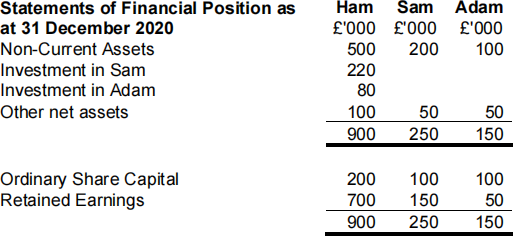

You have been asked by a friend, Elsa, who is new to the approaches of consolidated accounting to review her workings for the consolidation of the Ham Group. Ham plc acquired 70% of the ordinary shares of Sam Ltd and 30% of the ordinary shares of

Adam Ltd during the financial year. All three companies prepared financial statements at 31 December 2020 as follows:

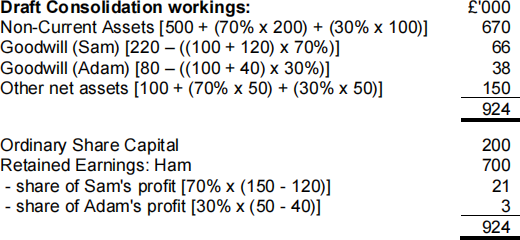

The retained earnings of Sam and Adam at the date of acquisition were £120,000 and £40,000, respectively. Elsa has produced the following draft Consolidated Statement of Financial Position (including her workings):

Explain how the acquisitions of Sam and Adam should be accounted for by Ham plc in accordance with applicable IASB accounting standards, and why the approach adopted by Elsa above does not accord with the Conceptual Framework’s concept of “Substance”. Your answer should also include the correct consolidated statement of financial position (and associated workings) in accordance with IASB accounting standards. However, the answer should focus on an explanation of the consolidation process in terms of the conceptual framework and applicable accounting standards,

and the application of “substance”. Recommended word count: 375 words

(Total 25 marks)

2. Provisions: Restructuring

Drum is an entity that prepares financial statements to 30 June each year.

On 30 April 2020, the directors decided to discontinue the business of one of Drum’s operating divisions. They decided to cease production on 31 July 2020, with a view to disposing of the property, plant and equipment soon after 31 August 2020.

On 15 May 2020, the directors made a public announcement of their intentions and offered the employees affected by the closure termination payments or alternative employment opportunities elsewhere in the group. Relevant financial details are as follows:

(a) On 30 April 2020, the directors estimated that termination payments to

employees would total £15 million and the costs of retraining employees who would remain employed by other group companies would total £1.5 million. Actual termination costs paid out on 31 July 2020 were £15.6 million and the latest estimate of total retraining costs is £700,000.

(b) Drum was leasing a property under a rental lease agreement that expires on 30

September 2022. On 30 June 2020, the present value of the future lease rentals (using an appropriate discount rate) was £6 million. On 31 August 2020 Drum made a payment to the lessor of £5.5 million in return for early termination of the lease. There were no rental payments made in July or August 2020.

(c) The loss after tax of Drum for the year ended 30 June 2020 was £14.4 million. Drum made further operating losses totalling £6 million for the two-month period

1 July 2020 to 31 August 2020.

Required:

Explain how the provision that is required in the financial statements of Drum at 30 June 2020 in respect of the decision to close is calculated.

Recommended word count: 375 words (Total 25 marks)

3. Conceptual Framework and Intangible Assets

The IASB’s Conceptual Framework, revised in 2018, identifies two fundamental qualitative characteristics that financial information requires to be useful to decision making: relevance and faithful representation. There is, however, a level of trade-off between these two characteristics. Despite internally-generated brands of global companies being worth billions (Apple’s brand is reported to be worth $323bn in 20201) these are not allowed to be included as internally-generated assets in the statement of financial position, under IAS 38 Intangible Assets. However, the same assets should be recognised, at fair value, if acquired by another entity under IFRS 3 Business Combinations.

Required

Discuss whether the qualitative characteristics of the IASB’s Conceptual Framework and the two accounting standards, IAS 38 and IFRS 3, meet the needs of the user, given increasing disparities between book values reported in companies’ Statements of Financial Position and their market capitalisation (value of their shares in the market).

Recommended word count: 750 words (Total 50 marks)

2022-01-25