BEO2010 – International Trade Practices

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

BEO2010 – International Trade Practices

Detailed Solutions for Questions 1–3

October 24, 2025

Question 1: Import Cost Calculation and Product Se- lection (10 marks)

Task

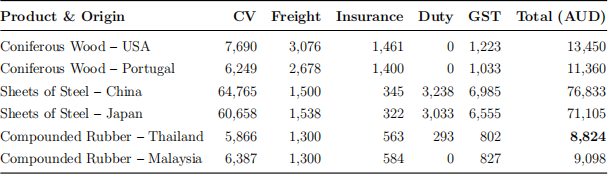

An Australian company plans to import one of six product—country combinations. The objective is to determine which product has the lowest total landed cost after customs clearance, including freight, insurance, duty, and GST.

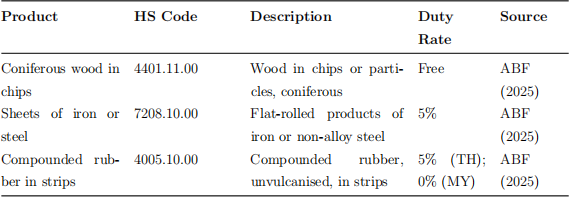

1.1 Tariff Classification and Duty Rates

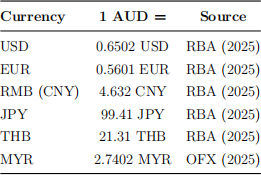

1.2 Exchange Rates (24 October 2025)

1.3 Calculation Method

VoTI = CV + Duty + Freight + Insurance

GST = 10% × VoTI

Total Landed Cost = CV + Freight + Insurance + Duty + GST

1.4 Calculation Results

Cheapest product: Compounded rubber (Thailand) — Total landed cost AUD 8,824.42.

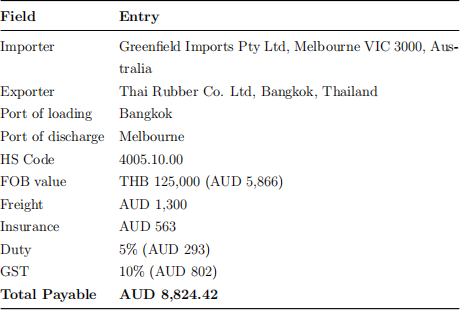

1.5 Import Declaration (N10)

Question 2: Forward Exchange Contract for Japanese Imports (10 marks)

Products: Matcha powder (840 kg @ 1,000 JPY/kg = 840,000 JPY); Sake (2,400 bottles @ 800 JPY = 1,920,000 JPY).

Total: 2,760,000 JPY.

Forward premium: 4.78%.

Payment: 30 days after shipment.

2.1 Decision

No forward contract is signed because the forward rate adds a 4.78% premium and the JPY is expected to weaken against the AUD, making spot settlement cheaper.

2.2 Exchange Rate Analysis

|

Week |

Rate (AUD/JPY) |

AUD Payable |

|

Week 1 (Spot) |

0.0090 |

24,840 |

|

Week 6 (Spot) |

0.0085 |

23,460 |

|

Week 6 (Forward, 4.78%) |

0.00943 |

26,039 |

Net Benefit = V (S6 - F) = 2,760,000 × (0.0085 - 0.00943) = -2,579 AUD

Interpretation: The forward contract would cost AUD 2,579 more. The company saves money by remaining unhedged.

2.3 Analysis

• Forward contracts fix exchange rates, removing uncertainty.

• They incur a cost when the domestic currency strengthens.

• A forward would be beneficial only if the JPY appreciates more than 4.78%.

• In this case, remaining unhedged provides a better financial outcome.

Question 3: Export Documentation – CIP Bangkok (10 marks)

Exporter: Greenes Pty Ltd, 1010 Key Street, Moorabbin VIC 3838, Australia.

Buyer: Chabang Imports, 10 Postbank St, Bangkok 10150, Thailand.

Payment: Letter of Credit.

Delivery Terms: CIP Bangkok (Incoterms 2020).

3.1 Product Values

|

Product |

Quantity |

Unit Price (AUD) |

Total (AUD) |

|

Australian Lamb (AULM) |

1,750 kg |

10.00 |

17,500 |

|

Australian Wine (AUWN) |

2,400 bottles |

8.00 |

19,200 |

|

FOB Total |

|

|

36,700 |

3.2 Transport Cost Comparison

|

Mode |

Freight (USD) |

Other Costs (AUD) |

Insurance (0.3%) |

|

Sea (Vista Voyage 112) |

800 × 1.53 = 1,224 |

470 |

121.11 |

|

Air (TG200) |

3,930 × 1.53 = 6,012.9 |

545 |

121.11 |

Selected Mode: Sea transport (Vista Voyage 112), cheaper by approximately AUD 4,864.

3.3 CIP Invoice Summary

• Vessel: Vista Voyage 112 (B/L No. BS1584)

• Departure: Melbourne (10 Oct 2025)

• ETA: Port Ranong (7 Nov 2025)

• Total CIP Value: AUD 38,515.11

• Insurance Premium: AUD 121.11

• Payment: Letter of Credit

• Documents: Commercial Invoice, Packing List, Bill of Lading, Insurance Certificate

3.4 Packing List

|

Product |

Boxes |

Gross Weight (kg) |

Vol (m3 /box) |

Total Vol (m3 ) |

|

Lamb |

35 |

1,750 |

0.30 |

10.5 |

|

Wine |

400 |

3,200 |

0.20 |

80.0 |

|

Total |

435 |

4,950 |

|

90.5 |

3.5 Summary

• Chosen Transport: Sea (Vista Voyage 112)

• CIP Invoice Value: AUD 38,515.11

• Insurance Premium: AUD 121.11

• Payment Method: Letter of Credit

• Delivery Term: CIP Bangkok (Incoterms 2020)

References

• Australian Border Force (2025). Tariff classification overview. Available at: https://www.abf.gov.au/importing-exporting-and-manufacturing/tariff-classification (Accessed 24 Oct 2025).

• Australian Border Force (2025). Schedule 3 – Chapter 40: Compounded rubber. Available at: https://www.abf.gov.au/importing-exporting-and-manufacturing/tariff-classification/current-tariff/schedule-3/section-vii/chapter-40 (Accessed 24 Oct 2025).

• Australian Border Force (2025). Schedule 3 – Chapter 44: Wood in chips or parti-cles. Available at: https://www.abf.gov.au/importing-exporting-and-manufacturing/tariff-classification/current-tariff/schedule-3/section-ix/chapter-44 (Accessed 24 Oct 2025).

• Australian Border Force (2025). Schedule 3 – Chapter 72: Iron and Steel Products. Available at: https://www.abf.gov.au/importing-exporting-and-manufacturing/tariff-classification/current-tariff/schedule-3/section-xv/chapter-72 (Accessed 24 Oct 2025).

• Reserve Bank of Australia (2025). Exchange Rates. Available at: https://www.rba.gov.au/statistics/frequency/exchange-rates.html (Accessed 24 Oct 2025).

• ANZ Bank (2025). Foreign Exchange Rates Popup. Available at: https://www.anz.com/aus/ratefee/fxrates/fxpopup.asp (Accessed 24 Oct 2025).

• OFX Group Ltd. (2025). Live and Historical Exchange Rates. Available at: https://www.ofx.com/en-au/forex-news/historical-exchange-rates/ (Accessed 24Oct 2025).

• International Chamber of Commerce (2020). Incoterms 2020: CIP (Carriage and Insurance Paid To). Paris: ICC Publications No. 723E.

• Customs Tariff Act 1995 (Cth). (as amended). Available at: https://lawlex.com.au/tempstore/consolidated/6832.pdf (Accessed 24 Oct 2025).

2025-11-01