BAFI1005 Financial Markets and Institutions Semester 2, 2025

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

BAFI1005 Financial Markets and Institutions - Group

Assignment (Stage 2)

Semester 2, 2025

Weighting: 20%

Overview

Your team works for a renowned FX trading company, Snowy River Ltd. The company specialises in trading major currencies such as the Australian Dollar (AUD), British Pound (GBP), Canadian Dollar (CAD), Euro (EUR), Japanese Yen (JPY), New Zealand Dollar (NZD), Swiss Franc (CHF) and US Dollar (USD). The company also trades various foreign exchange-related derivatives for its clients. In addition, it provides general advice to other clients who trade for themselves. The firm’s chief trading executive, Jayden Yap, has requested your team’s expertise in trading foreign currencies in order to improve the firm's trading strategy and profits. You have been asked to prepare a detailed report in this regard. In your report you must address the following scenarios:

Part 1 Speculation [5 marks]

Use the three/four market views developed by your team in stage 1, and use the market views to devise speculation strategies that enable your organisation to take advantage of your predicted changes in exchange rates. You should specify which currencies you will buy or sell. As part of your strategy, you must create a portfolio and this portfolio will comprise of the currency pairs analysed in your market view.

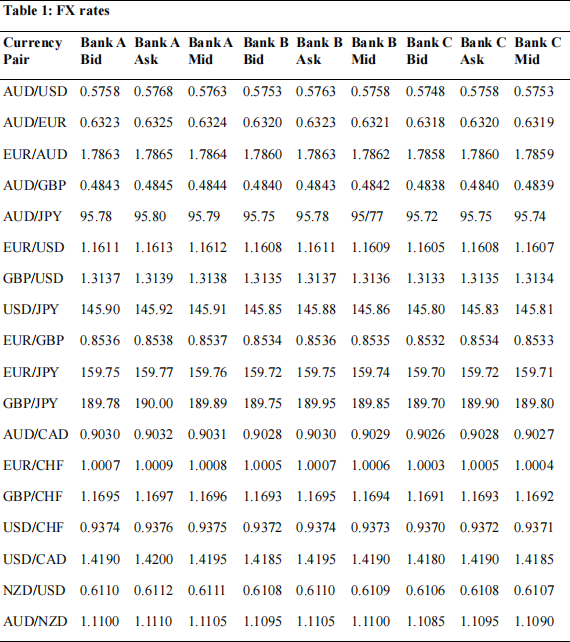

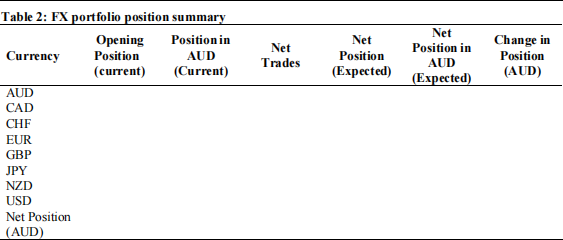

The senior management has allocated you 400,000,000 units of each currency as the initial balance for your speculation strategy if you are speculating on AUD, GBP, CAD, EUR, NZD, CHF or USD and 25,000,000,000 units if you are speculating on JPY. For instance, if you are speculating on AUD/EUR and decided to short the EUR, then you have been allocated 400,000,000 EURs for this purpose. The corresponding long/short position should be calculated using bid/ask rates provided in Table 1. Please note that you must speculate on ALL currency pairs based on your stage 1 market view. You must then take long and short positions in the respective currencies in accordance with your market view as a price taker. In the report, you are requested to provide a brief summary of your market views before demonstrating your long/short speculation strategy. [2 Marks]. These long and short positions will constitute your portfolio’s current opening position. Based on your initial position you must choose the most appropriate quotations among Bank A, B and C in Table 1, and estimate the opening AUD value of your portfolio using the corresponding mid rates and update your position summary table below with your speculative position [3 Marks]. Mid rate = (bid rate + ask rate)/2

Part 2 Risk Assessment [7 marks]

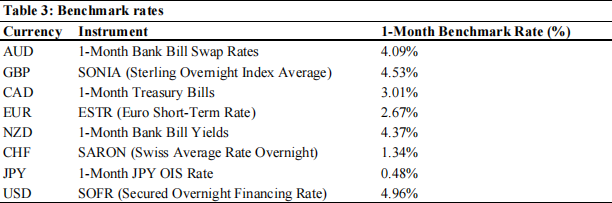

Senior management is concerned about the recent developments in the financial markets. There is a general belief that market volatility has been relatively high, yet it might climb even higher than expected in the near future. You have been asked to conduct a thorough risk assessment of your speculative positions undertaken in Part 1. For this purpose, the firm’s foreign currency analyst has provided you with the 1-month benchmark rates of these major currencies.

Using the interest rates in Table 3, calculate the implied forward bid, ask and mid rates for the THREE OR FOUR currency pairs you selected [1 Marks]. You must then calculate the value of your FX portfolio using the calculated bid/ask rates. Report the expected value of your position in each currency in the position summary in Table 2 [2 Marks].

Finally, you must calculate the expected profit/loss (gain or loss over the opening position) on your portfolio in AUD [2 Mark]. The AUD value of the net expected position must be calculated using the estimated mid rates.

Explain your final portfolio position to the senior manager.

Discuss whether your speculative positions will generate profits for the company. You must explain ending positions for each currency (and it’s AUD value using mid rates) in your portfolio? Does your portfolio have any exposure to exchange rate risk? What recommendations, if any, will you make to the senior management? [2 Mark].

Part 3 Arbitrage [6 marks]

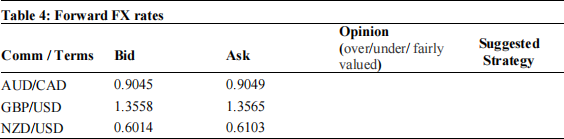

The firm’s senior management has taken note of your expertise in arbitrage trading. You have been asked to identify potential arbitrage opportunities based on the differences in implied forward rates and actual forward rates. Suppose that the actual forward rates are as presented in Table 4.

Calculate the implied forward rates for the given three pair currencies, and inform the company whether the commodity currencies listed in Table 4 are over-, under-, or fairly valued compared to the implied forward rates you calculated [2 Marks], and which bank will you trade with and what is your suggested strategy to the top management (buy or sell the commodity currency)? [1 Marks].

If there is any arbitrage opportunity available between the implied forward rates and the actual forward rates listed in Table 4, how much profit can you generate for the company as a price taker with 50,000,000 units of currency (choose the most profitable option) [2 Marks]. To minimise the transaction costs involved you can only exploit arbitrage opportunities between two exchange rates (i.e., NO TRIANGULAR ARBITRAGE OPPORTUNITY ALLOWED). Finally, you must convert profit, if any, to AUD using the mid rates estimated in implied forward rates [1 Mark].

Note: Indicate long positions with a positive sign and short positions with a negative sign (e.g. a short position of 45,000,000 GBP should be indicated as --45,000,000). Mid rate = (bid rate + ask rate)/2

Formatting & Presentation [2 marks]

The report must be professionally presented using Times New Roman, size12 font, double-spaced for the main text, and single spaced for tables, figures & appendices. Figures and graphs should be clearly labelled and numbered. Any information obtained from sources external should be referenced according to AGPS Harvard Style or APA style. A word limit of maximum of 3000 words applies with a tolerance of + 10%, excluding appendices and tables.

Submission

1. Students are required to register their groups online via Canvas.

2. Go to the course site on Canvas. Submit your assignment under the submission point. Only one submission is required per group. It’s the responsibility of the group members to ensure that the assignment is submitted on time.

3. The report must have the university prescribed cover sheet and the following details:

• Student names and student numbers of those who have contributed to the report

• FX Session attended

• Assignment Group Number

• Name ofFX Session Instructor

2025-09-23