ECON455: Behavioral Economics

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECON455: Behavioral Economics

Reminders:

No late work will be accepted.

Answers must be submitted prior to the published deadline as a single pdf document.

Answers must show the steps that proceed final calculations and must be original work.

It is vitally important that your work is legible. Unreadable work will not be graded and will not be awarded any credit. If your original homework is on paper, consider using one of many free scanning apps: https://kb.wisc.edu/luwmad/83070

Students are required to include the names of any peers they collaborate with on an assignment.

Q1: Nudge Terminology (1 point)

Demonstrate your understanding of this week's reading by describing/defining each of the following terms. Explain the meaning of the term and how the idea is employed in the context of economic decision-making. Give an example of where and how each might be observed in the 'real-world'

Anchoring

Availability

Representativeness

Framing

Priming

iNUDGES

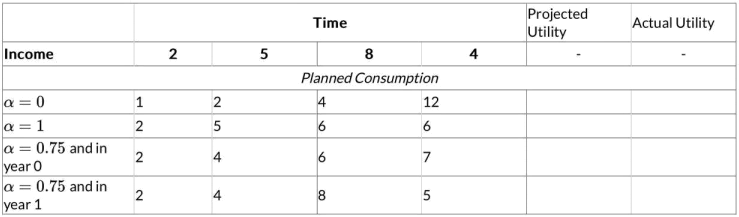

Q2: Table 10.5 from Behavioral Economics (1 point)

Review Table 10.5 from the textbook. Use the model of Projection Bias introduced in Section 10.6 to complete the following table for a representative agent (lan):

Recall that in this model, the representative agent's utility function is:

where ct is consumption and  and projection bias (α) impacts lan's habituation level via the equation

and projection bias (α) impacts lan's habituation level via the equation

Q3: Save More Tomorrow (1 point)

In reading the book Nudge, we learned that Americans' retirement savings are "woefully low, if not zero". In fact, 2005 marked the first year that Americans' personal savings rate turned negative since the Great Depression. Why do Americans save so little for retirement? One explanation might be that they are unaware of what resources will be needed later in life and thus are uninformed. This hypothesis fails, however, when Americans are surveyed and acknowledge that they are aware of the problem. Studies have found that as many as 68 % of 401(k) plan participants report their savings rate as "too low" and only 1% of participants gauge their savings as "too high". Using this information, answer the following questions:

A. If Americans know they are saving too little for retirement, why don't they save more? What are the structural impediments they face and what are the behavioral factors acting against them? ( point)

point)

B. Richard Thaler and Shlomo Benartzi developed a choice architecture plan called "Save More Tomorrow". Explain this plan and the psychological principles that underlie its design. Using the language of behavioral economics, explain why this program might be expected to produce better results than regular savings plans - like an IRA or a 401(k). ( point)

point)

2025-07-18