07 33109 LH Advanced Macroeconomics

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

07 33109

LH Advanced Macroeconomics

MOCK EXAMINATION 2021/22

Section A: Answer ONE of the following two questions

1. Consider a model of firm-level investment which allows for convex capital adjustment costs. Assume that the depreciation rate is zero in order to simplify our analysis. We can show that the following expression holds as an equilibrium condition in this model:

C is an adjustment cost function which satisfies C(0)=0, C′(0)=0 and C′′(•)>0, where C′ and C′′ are the first and second partial derivatives of C with respect to investment (It), respectively. Furthermore,  where r is the real interest rate and

where r is the real interest rate and ![]()

![]() is the Lagrange multiplier of the representative firm’s constrained optimisation problem at time t.

is the Lagrange multiplier of the representative firm’s constrained optimisation problem at time t.

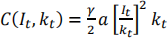

Assume that the aforementioned adjustment costs depend on the level of capital employed by the representative firm and that they are quadratic in investment in the following way:

where y > 0 and a > 0 are parameters.

Answer the following questions:

a) Provide an economic interpretation for the equilibrium condition above (equation 1). Explain the meaning of qt as part of your answer. [10%]

b) Verify that the adjustment cost function above (equation 2) is convex in It. Explain intuitively why these adjustment costs are needed in the model. [20%]

c) Compute the equilibrium condition considered in part (a) when equation (2) is used to model capital adjustment costs. Rearrange your answer so that It/kt appears on the left-hand side. Summers (1981) sets ![]() = 1 and uses this expression to construct an estimating equation which he then applies to US data for the period 1931-1978. Why are Summers’ findings problematic for the model of investment with convex adjustment costs considered in this question? [40%]

= 1 and uses this expression to construct an estimating equation which he then applies to US data for the period 1931-1978. Why are Summers’ findings problematic for the model of investment with convex adjustment costs considered in this question? [40%]

d) Explain the difference between ‘marginal q’ and ‘average q’ and discuss why this distinction is important when evaluating the theory against real-world data. Use some relevant empirical evidence to support your answer. [30%]

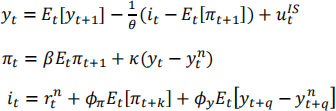

2. Consider a forward-looking New Keynesian (NK) model written in the following form:

where ![]()

![]() +

+![]() is the natural log of real output in time period t+q;

is the natural log of real output in time period t+q; ![]()

![]() is the nominal interest rate at time t;

is the nominal interest rate at time t; ![]()

![]() +

+![]() is the rate of inflation in time period t+k;

is the rate of inflation in time period t+k; ![]()

![]()

![]() is the natural log of the economy’s ‘natural’ (i.e. long-run) level of output, such that [

is the natural log of the economy’s ‘natural’ (i.e. long-run) level of output, such that [![]()

![]() +

+![]() −

− ![]()

![]()

![]() ] can be interpreted as the output gap in time period t+q;

] can be interpreted as the output gap in time period t+q; ![]()

![]() is the natural rate of interest at time t. A mean-zero shock has been added to equation (3),

is the natural rate of interest at time t. A mean-zero shock has been added to equation (3), ![]()

![]() , which is assumed to follow an independent AR(1) process.

, which is assumed to follow an independent AR(1) process.

The expectations operator (![]()

![]() ) is required for future variables; we assume that all agents in the model possess rational expectations. The Calvo (1983) model of price adjustment has been employed on the supply-side of the model and labour is the only input to production. There is no government spending or international trade in this theoretical framework. Finally, the following parameter restrictions are imposed:

) is required for future variables; we assume that all agents in the model possess rational expectations. The Calvo (1983) model of price adjustment has been employed on the supply-side of the model and labour is the only input to production. There is no government spending or international trade in this theoretical framework. Finally, the following parameter restrictions are imposed: ![]() >

>

0; ![]() > 0 , 0 <

> 0 , 0 < ![]() < 1,

< 1, ![]()

![]() > 0 and

> 0 and ![]()

![]() ≥ 0.

≥ 0.

Answer the following questions:

a) Assume that k=q=-1 in equation (5). Explain intuitively – i.e. without mathematical derivations – the importance of ![]()

![]() to the equilibrium outcome of the model. Provide some relevant empirical evidence to support your answer. [20%]

to the equilibrium outcome of the model. Provide some relevant empirical evidence to support your answer. [20%]

b) Now assume that k=q=1 in equation (5). Explain intuitively – i.e. without mathematical derivations – the importance of ![]()

![]() to the equilibrium outcome of the model. Provide some relevant empirical evidence to support your answer. [20%]

to the equilibrium outcome of the model. Provide some relevant empirical evidence to support your answer. [20%]

c) Consider the model proposed by Krugman (1998), which allows for the possibility of a ‘liquidity trap’. Use a diagram to show how monetary policy, implemented through the nominal money supply, can be ineffective in this theoretical framework. [40%]

d) What can the central bank do to regain influence over economic outcomes? Use relevant real-world examples to support your answer. [20%]

Section B: Answer ONE of the following two questions

3.

Discuss how the introduction of money in an overlapping generations model leads to the attainment of superior economic outcomes.

4.

Discuss and assess the practical importance of Ricardian equivalence for the conduct of fiscal policy.

2021-12-26