ACCFIN4070 Corporate Finance

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Subject of Accounting and Finance

Degree of BAcc

Degree Exam

Corporate Finance, ACCFIN4070

![]()

SECTION A

You must answer two questions from this section.

Please use ONE WHITE answer sheet per question. If there is not enough space on a white sheet, please raise your hand to request a YELLOW answer sheet in order to continue your answer.

QUESTION 1

UGAF management team is meeting to decide on a new corporate strategy. There are four options, each with a different probability of success and total firm value in the event of success, as shown below:

Strategy

A B C D

Probability of Success 100% 80% 60% 40%

Firm Value if Successful (in $ million) 50 60 70 80

Assume that for each strategy, in the event of failure firm value is 2 (salvage value).

1.1 For each strategy, calculate the overall expected payoff and the expected payoff for equity holders. Specifically, fill in the blanks (16 in total) in the following table.

A B C D

Expected Payoff ? ? ? ?

Debt Face Value (D)

0

20

40

|

Expected Equity Value A B C D |

|

? ? |

(12%)

1.2 Suppose the management team will choose the strategy that leads to the highest expected value of its equity. Which strategy will management choose in response to the three different levels of debt face value in Q1.1?

(3%)

1.3 What type of agency costs of debt is illustrated in your answer to Q1.2? What is the amount of such costs?

(5%)

Now consider the scenario that UGAF has debt with a face value of 40 outstanding. Assume that all risk is idiosyncratic, the risk-free rate is 3%, and there are no taxes. Suppose UGAF is considering to issue equity and buy back its debt, reducing the debt’s face value to 5.

1.4 If it does so, what strategy will it choose after the transaction? Is this transaction value enhancing?

(4%)

1.5 With this recapitalization to reduce leverage, show the net gain/loss for equity and debt holders, respectively. Do you expect the management team to choose to reduce its leverage? This example illustrates the leverage ratchet effect. Briefly explain what it is.

(9.3%) (TOTAL 33.3%)

QUESTION 2 (PLEASE USE A NEW WHITE ANSWER SHEET)

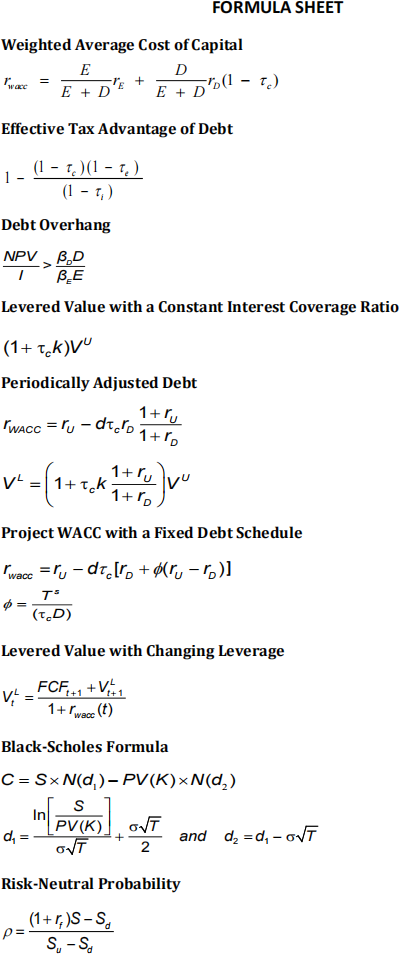

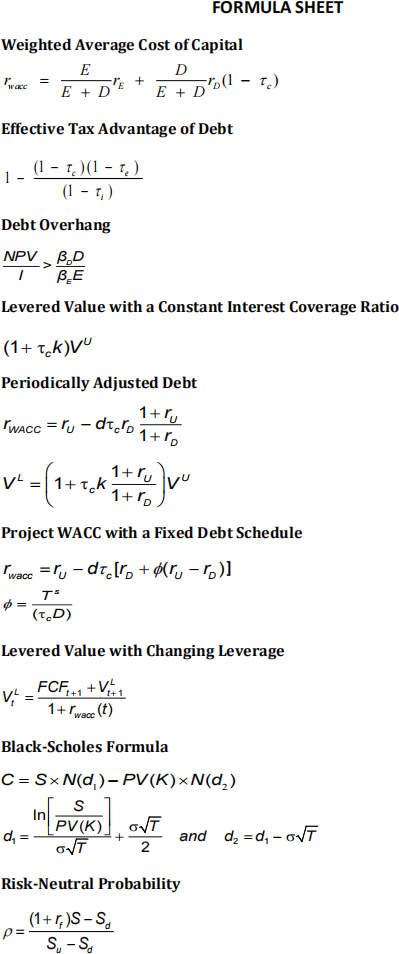

XL Systems is expected to generate free cash flows of $24 million per year. XL has permanent debt of $80 million, a corporate tax rate of 40%, and an unlevered cost of capital of 12% and its cost of debt capital is 6%.

2.1. What is the value of XL's equity using the Adjusted Present Value (APV) method?

(6%)

2.2. What is the value of XL's equity using the Weighted Average Cost of Capital (WACC) method?

(8%)

2.3. What is the value of XL's equity using the Flow-to-Equity (FTE) method?

(6%)

2.4. Compare between these three methods for valuing levered investments: WACC, APV, and FTE. Use the XL example above to support your answer.

(13.3%) (TOTAL 33.3%)

SECTION B

You must now answer one question from this section. As before, please use a new WHITE answer sheet. If there is not enough space on a white sheet, please raise your hand to request a YELLOW answer sheet in order to continue your answer.

QUESTION 3 (PLEASE USE A NEW WHITE ANSWER SHEET)

A. The quarterly working capital levels for HappyShoes are presented in the following table:

Quarter 1 2 3 4

Cash 605 625 175 1000

Accounts Receivable 585 745 1260 760

Inventory 410 540 725 375

Accounts Payable 835 910 1055 1145

3.1. What are the permanent working capital needs for HappyShoes? What are the

temporary working capital needs?

(6%)

3.2. Explain the matching principle. Why might a company choose to finance permanent

working capital with short-term debt? What is it called for such a policy?

(12%)

B. Corporate governance – the system of controls, regulations, and incentives designed to prevent fraud – is a story of conflicts of interest among stakeholders and attempts to minimize them.

3.3. In the absence of monitoring, one way to mitigate the conflict of interest between manager and owners is through tying managerial compensation to performance. What are the advantages and disadvantages of increasing the options granted to CEOs? Is it necessarily true that increasing managerial ownership stakes will improve firm performance? Provide academic references to support your answer.

(15.3%) (TOTAL 33.3%)

QUESTION 4 (PLEASE USE A NEW WHITE ANSWER SHEET)

A. Your firm can invest in a risk-free technology that requires an up-front investment of $1 million. You are hesitant to invest because of uncertainty over future interest rates. Suppose that all interest rates will be either 8% or 4% in one year and remain there forever. The risk-neutral probability that interest rates will drop to 4% is 40%. The one- year risk-free interest rate is 5% and today's rate on a risk-free perpetual bond is 6%. The rate on an equivalent perpetual bond that is repayable at any time (the callable annuity rate) is 7.65%.

Assuming that this project will provide your firm with perpetual annual cash flows of $65,000.

4.1. Would you be better off if you wait and invest in the project next year rather than

investing in the project today? Support your answer with NPV calculation.

(6%)

4.2. Verify that the hurdle rate rule of thumb gives the correct time to invest in this case. (4%)

4.3. To evaluate real options in the capital budgeting decision, two commonly used rules of thumb in practice are the profitability index and hurdle rates. Explain what they are and the type of uncertainty that they account for the option to wait.

(7%)

B. Two major categories of long-term financing are equity and debt.

4.4. The process of selling stock to the public for the first time is called the initial public offering (IPO). List and discuss two characteristics about IPOs that financial economists find puzzling. Provide academic references to support your answer.

(10%)

4.5. List and compare four types of corporate debt that are typically issued.

(6.3%) (TOTAL 33.3%)

2021-12-15