ECON339 Applied Financial Modelling Mid-Semester Examination Paper Spring 2022

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECON339

Applied Financial Modelling

Mid-Semester Examination Paper

Spring 2022

Q1. Briefly describe the criterion used to obtain the ordinary least square estimator. [2]

|

The model must be linear in the parameters.The Gauss-Markov theorem is applied and the estimator for ols is the best linear unbiased estimate (BLUE). |

Q2. When estimating a regression in a sample why is a large sample observations preferred to a small sample? [2]

|

This means that the estimates will converge to their true values when the sample size is larger. |

Q3. Why is an efficient estimator a desirable property of the OLS estimator? [2]

|

When the estimate is valid and can minimise the probability of it being far from the true value. |

Q4. State the assumption(s) under the classical linear regression model giving rise to a biased standard error of the coefficient estimates when violated. [2]

|

The bias is due to the omission of any of the variables associated with the dependent and independent variables. |

Tt = a + bTM,t + ut (1)

Tt = c + dTM,t + evolt + vt (2)

where Tt is stock returns, TM,t is market returns, and volt is market volatility. State the null hypothesis if regression (1) is nested in regression (2). [2]

|

H0: b=d=e=0 |

Q6. Holding other things constant, what is the effect of (a) sample size and (b) variation in x on the variance of the OLS estimator? [2]

|

a :An increase in sample size will lead to a decrease in the OLS estimator. b:An increase in variation in x will result in an increase in the OLS estimator. |

Use the following information to answer Q7-Q9.

A researcher runs the following regression with the Eviews output presented below.

nettfa = b0 + b1 inc + b2 age + b3marr + b4male + e (3)

where

nettfa = the net financial wealth (measured in $’000)

inc = income

age = the age of the respondent

marr = a dummy variable equals 1 if the respondent is married and 0 otherwise. male = a dummy variable equals 1 if the respondent is male and 0 otherwise.

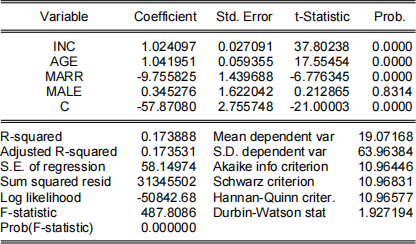

Dependent Variable: NETTFA

Method: Least Squares

Date: 08/23/22 Time: 19:06

Sample: 1 9275

Included observations: 9275

Q7. Interpret the coefficient of age. [2]

|

Net financial wealth increases by 1.041951 * 1000 per age increase. |

Q8.State the independent variable whose estimate is not statistically significant at the 5% significance level. [2]

|

MALE, p-value >0.05. |

Q9. On average is there any gendre bias in the net financial wealth in the sample? [2]

|

There are biases and men have more wealth |

Use the following information to answer Q10-Q12.

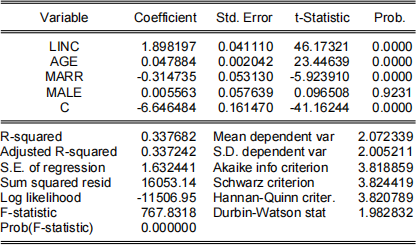

The researcher estimated a log-log regression and the output is reported below:

log (nettfa) = b0 + b1 log (inc) + b2 age + b3marr + b4male + e (4)

Dependent Variable: LNETTFA

Method: Least Squares

Date: 08/23/22 Time: 19:04

Sample: 1 9275

Included observations: 6029

Q10. Between equations (3) and (4), which model do you prefer? Explain. [2]

[Hint: the included observations in regression 4 are far lesser than the sample in regression 3]

|

equations (4) Because in (4) the square of r and the square of the adjusted r are higher |

Q11. Interpret the coefficient of log(inc) . [2]

|

Net financial wealth increases by $1,898 with every $1,000 increase in income. |

Q12. Interpret the coefficient of marr . [2]

|

For each unit increase in marr ,nettfa will decrease by 0.31% . |

Use the following information to answer Q13-Q14.

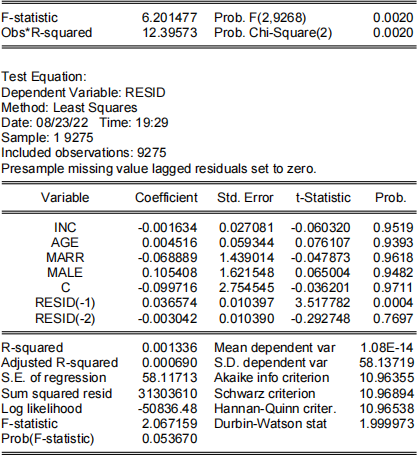

The researcher performed diagnostic tests on the residuals of regression (3).

Breusch-Godfrey Serial Correlation LM Test:

Null hypothesis: No serial correlation at up to 2 lags

Q13. Based on the Breusch and Godfrey test, what is the order of the lag of the serial correlation in the null hypothesis? [2]

|

Second-order autocorrelation. |

Q14. What can you infer from the Breusch and Godfrey test results? [2]

|

There is an autocorrelation problem because the p-value is not significant and reject Null hypothesis |

Use the information below to answer Q15 to Q17.

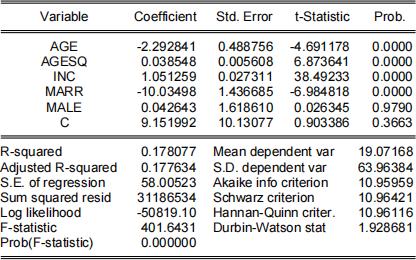

The researcher is interested in a nonlinear relationship between nettfa and age. The squared of age (denoted agesq) is incorporated in regression (3) and the regression output is shown below.

nettfa = b0 + b1 inc + b2 age + b3 age2 + b4marr + b5male + e (5)

Dependent Variable: NETTFA

Method: Least Squares

Date: 08/23/22 Time: 20:14

Sample: 1 9275

Included observations: 9275

Q15. Between models (3) and (5), which is the preferred model? Explain. [2]

|

I chose 3 because 3 has fewer independent variables than 5 and they are significantly correlated |

Q16. At what age is the net financial wealth maximised? Show your working. [2]

Q17. State the name of the test that you can perform to determine whether a linear regression or a nonlinear regression is a better fit for the data. [2]

|

T-test |

Use the information below to answer Q18 to Q20.

The researcher performed a test for heteroskedasticity on residuals of equation (3). The table below shows the results.

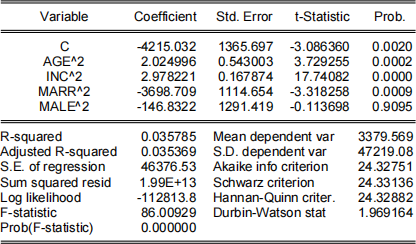

Heteroskedasticity Test: White

Null hypothesis: Homoskedasticity

Test Equation:

Dependent Variable: RESID^2

Method: Least Squares

Date: 08/23/22 Time: 20:24

Sample: 1 9275

Included observations: 9275

Q18. What can you infer from the White test result? [2]

|

There is no heteroscedasticity. |

Q19. Which property of the OLS estimator is violated based on the White test result? [2]

|

MALE^2 |

Q20. State an alternative method of estimating regression (3) that will address the concern of Q19. [2]

|

Weight Least Square (WLS) Replacing the original model with a logarithmic model |

2024-04-29