ECMT 6002/6702: Econometric Applications

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECMT 6002/6702: Econometric Applications

1. Practice problems

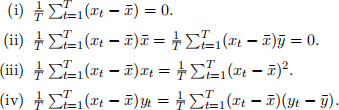

1. (Some basic algebra related to the OLS estimator) Suppose that observations (y1, . . . , yT) and (x1, . . . , xT ) are given and define

Verify the following:

Consider the following simple linear regression model:

yt = α + βxt + ut

(v) Show that the OLS estimator is given by

2. (Simple linear regression)

(i) Consider the following simple linear regression model:

yt = α + βxt + ut

Let ( ,

,  ) be the OLS estimates and

) be the OLS estimates and  . Verify that the sample average of

. Verify that the sample average of  is exactly equal to zero.

is exactly equal to zero.

(ii) Now consider the following regression model:

yt = βxt + ut

and let  be the OLS estimate and

be the OLS estimate and  . Is the sample average of

. Is the sample average of  still equal to zero?

still equal to zero?

(iii) Now consider the following regression model:

where

Let  be the OLS estimate and

be the OLS estimate and  . Show that the OLS estimate

. Show that the OLS estimate  is equivalent to

is equivalent to  b in (i) and thus the sample average of

b in (i) and thus the sample average of  is equal to zero.

is equal to zero.

(iv) Based on the results obtained in (i)-(iii), explain the role of the intercept.

2 Empirical application

Suppose that we are interested in the relationship between # of crimes and # of employed police officers on campus. The following model is considered:

Instructions:

1. Use the attached dataset. The dataset is considered in Wooldridge’s text book “Introductory Econometrics” and was collected from the FBI Uniform Crime Report.

2. Check summary statistics for yt and xt . If you are using R, use summary(y) and summary(x) if y and x are the vectors contain the observations.

3. Compute the OLS estimates of α and β. In R, lm(y ∼ x) can be used. You can easily do this in any statistical package but, I would recommend you compute those by your own code (see (1.2)). Depending on which software is used, the estimates can be slightly different. But they must be close to the following obtained by lm(y ∼ x) in R:

4. This computing exercise is not mandatory; any computing code related to this application will not be asked in the exams. But you are strongly encouraged to work on this by yourself with your preferred statistical software (this will be helpful for your assignments).

2024-02-25