Corporate Finance (FIN 213) Fall 2023 MIDTERM EXAM

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Corporate Finance (FIN 213)

Fall 2023

MIDTERM EXAM

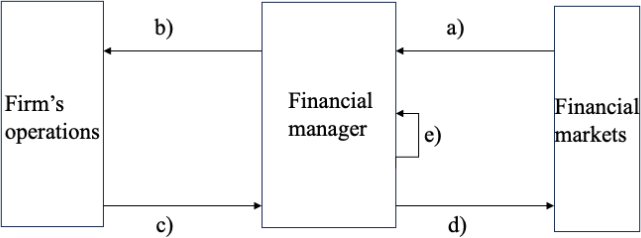

1. (10 points) The graph below illustrates the flow of cash for a corporation as it relates to the financial manager. In your own words, briefly provide an explanation for what a, b, c, d, and e represents.

a) Cash is raised by selling financial assets to investors (e.g., equity investors, bond holders, banks).

b) Cash is invested in the firm’s operations and is used to purchase assets. The financial manager makes capital budgeting decisions.

c) The firm’s operations/projects generates free cash flows.

d) A decision is made to return cash to investors (e.g., stock buybacks, dividends).

e) A decision is made to reinvest cash back into the firm for ongoing or future operations/projects.

2. (16 points) Briefly explain the Capital Asset Pricing Model (CAPM). Explain how the beta in CAPM relates to the concept of systematic and idiosyncratic risk. Should investors be compensated for exposure to systematic or idiosyncratic risk?

Under CAPM, E[r![]() ] = rf + B

] = rf + B![]() 'E[rm ] − rf )

'E[rm ] − rf )

In other words, the expected return on a risky asset, i, is the sum of (i) the risk-free rate of return and (ii) the asset’s beta multiplied by the market risk premium.

One way to think of beta is the covariance of the asset’s returns with the market’s returns, over the variance of the market’s returns. Returns are related to exposure to systematic risk, or market risk, under CAPM.

Investors are compensated for taking on systematic risk and not idiosyncratic risk, which can be reduced by diversification.

3. (15 points) Briefly compare and contrast the WACC method and APV method used in the valuation of projects/firms.

The WACC method calculates NPV by discounting free cash flows of a project/firm using the weighted average cost of capital as the discount rate. The effects of interest tax shields are incorporated in the WACC (discount rate). Note the tax rate term in WACC = (E/V) x r_e + (D/V) x (1 – tax rate) x r_d.

To calculate the NPV of a project/firm under the APV method, we separately calculate the (i) the NPV of the project/firm as if it was “all-equity” financed (base-case NPV) and (ii) the present value of financial side effects, such as interest tax shields. Then, we add the two components together.

A potential advantage of the APV method over the WACC method is in instances where financial side effects are complex. For example, in a LBO calculation (versus a simple recapitalization exercise), the leverage policy of the firm may change considerably in a relatively short period, causing interest tax shields to vary.

4. (7 points) Widget Inc. is considering a project that will require an initial outlay of $1,000 and will generate the following incremental free cash flows. Assume the discount rate is 10%. (If you need to make assumptions, state the assumptions clearly and briefly justify when applicable.)

Year 1: $300

Year 2: $400

Year 3: $500

a. (2 points) What is the NPV of the project?

NPV = -1000 + 300/1.1 + 400/1.1^2 + 500/1.1^3 = -21.04

b. (1 point) Under the NPV approach, should Widget Inc. undertake the project?

NPV<0, so Widget Inc. should not undertake the project.

c. (4 points) Suppose that after year 3, free cash flows are projected to grow at a steady 1% per year in perpetuity. For example, year 4 cash flows are $500 x 1.01 = $505 and year 5 cash flows are $505 x 1.01 = $510.05. What is the NPV of the project under the new assumptions? [Hint: Use perpetuity formula]

NPV = -1000 + 300/1.1 + 400/1.1^2 + 500/1.1^3 + (505/(0.10-0.01))/1.1^3 = 4194.67

5. (24 points) Kiwi Inc. is considering purchasing a new piece of equipment that will help boost the company’s sales of its pre-existing KPhones by $1000 each year and reduce costs by $100 each year. The new equipment will cost $2,100 to acquire. Assume this equipment has a two-year life and uses a straight-line depreciation method, in which it will depreciate to 0 at the end of year 2. The pre-tax salvage value of the equipment in year 2 will be $10 when sold. Moreover, the equipment will allow Kiwi Inc. to carry $15 less in inventory, beginning immediately at the end of year 0, and Kiwi Inc. will be able to further reduce its inventory by an additional $5 in year 1. In year 2, however, Kiwi Inc. will need to return its inventory to its original levels when the equipment is sold.

Kiwi Inc.’s corporate tax rate is 25%.

Kiwi Inc.’s cost of debt is 6%, equity beta is 1, and D/E ratio is 1.

Assume the risk-free rate is 4% and the market risk premium is 8%. Suppose Kiwi Inc. will use its WACC as the discount rate to evaluate the project. (If you need to make assumptions, state the assumptions clearly and briefly justify when applicable.)

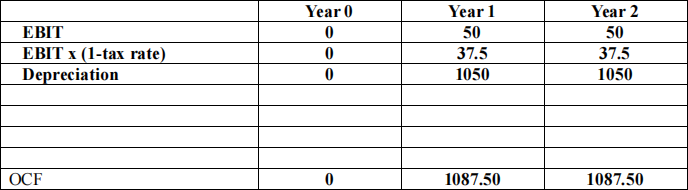

a. (3 points) What is Kiwi Inc.’s additional depreciation for each of the next two years? [Hint: Depreciation expense = annual depreciation rate x (Cost – BV at salvage)]

Using straight line depreciation, the depreciation rate each year for the two-year asset will be 50%.

Depreciation = Depreciation rate x (Cost – BV at salvage) = 0.5 x (2100 – 0) = 1050

b. (3 points) Using your answer from part (a), complete part of the following pro forma statement for the investment by Kiwi Inc.

EBIT = Sales – Costs – Depreciation

c. (2 points) How much in taxes does Kiwi Inc. save each year because of its ability to expense the depreciation from this new investment (depreciation tax shield)? [Hint: Depreciation tax shield = depreciation expense x tax rate]

Depreciation tax shield = depreciation expense x tax rate = 1050 x 0.25 = 262.50

d. (3 points) Using your pro forma from part (b), calculate the operating cash flows for each year. (Empty rows are provided for you to show work. You may not need all the additional space given.)

OCF = EBIT x (1-tax rate) + depreciation

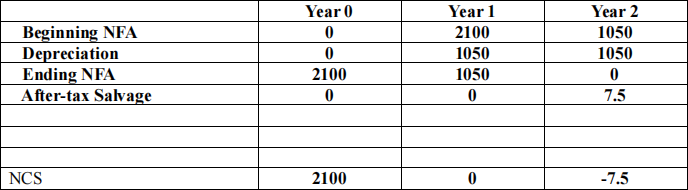

e. (4 points) Calculate the net capital spending for each year. (Empty rows are provided for you to show work. You may not need all the additional space given.) [Hint: After- tax salvage value = MV of asset sold – tax rate x (MV – BV of asset sold), where MV = market value and BV = book value]

NCS = Ending net fixed assets – beginning net fixed assets + depreciation – after tax gains from selling fixed assets

After-tax salvage value = MV – tax rate x (MV – BV)

At the end of year 2, after-tax salvage = 10 – 0.25 x (10 – 0) = 7.5

f. (2 points) Calculate the change in net working capital for each year. (Empty rows are provided for you to show work. You may not need all the additional space given.)

[Hint: Consider inventory as a current operating asset]

|

|

Year 0 |

Year 1 |

Year 2 |

|

Prior NWC |

0 |

-15 |

-20 |

|

Current NWC |

-15 |

-20 |

0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Change in NWC |

-15 |

-5 |

20 |

Change in NWC = Current NWC – Prior NWC

NWC = Current operating assets – current operating liabilities

g. (3 points) Calculate the free cash flows for each year. (Empty rows are provided for you to show work. You may not need all the additional space given.)

|

|

Year 0 |

Year 1 |

Year 2 |

|

OCF |

0 |

1087.50 |

1087.50 |

|

NCS |

2100 |

0 |

-7.5 |

|

Change in NWC |

-15 |

-5 |

20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FCF |

-2085 |

1092.5 |

1075 |

FCF = OCF – NCS – Change in NWC

h. (2 points) What is Kiwi Inc.’s WACC? [Hint: You can find cost of equity from beta equity using CAPM]

WACC = (D/V) x r_d x (1-tax rate) + (E/V) x r_e = 0.5 x 0.06 x 0.75 + 0.5 x 0.12 = 0.0825

Beta_e = 1 à Under CAPM, r_e = rf + Beta_e x MRP = 0.04 + 1 x 0.08 = 0.12 r_d = 0.06

D/E = 1 à D/V = E/V = 1/2

rf = 0.04 and MRP=0.08

i. (2 points) What is the NPV of this project? Should Kiwi Inc. undertake the project?

NPV = -2085 + 1092.5/1.08 + 1075/1.08^2 = -151.79 à No, since NPV<0

NPV = -2085 + 1092.5/1.0825 + 1075/1.0825^2 = -158.37 à No, since NPV<0

6. (12 points) Suppose Great Widgets Inc. recently acquired Better Gadgets Inc. Before the

acquisition, Great Widgets Inc. only had one division – the service division. After the

acquisition, Great Widgets Inc. has two divisions, the service division and the product

division (formerly known as Better Gadgets Inc.). Suppose the current total value of Great

Widgets Inc. is three times the net present value of projected free cash flows from the product division. For each division, its net present value is calculated by discounting expected free cash flows using its respective WACC. Assume neither division has excess cash or liabilities that are immediately due. The company and its divisions currently have no debt (D/E=0).

Assume the risk-free rate is 4% and the market risk premium is 8%. The company’s corporate tax rate is 0.

Suppose we know the following for the service division:

• Projected Year 1 FCF = $500,000

• Projected free cash flows are perpetual and constant (no growth)

• The service division never had any debt

Suppose we know the following for the product division (formerly Better Gadgets Inc.):

• Projected Year 1 FCF = $100,000

• Projected free cash flows are perpetual, growing at a steady annual rate of 2%

• Historically, Better Gadgets Inc. has a D/E ratio of 1. Better Gadgets Inc. historically has an equity beta of 1 and a cost of debt of 4%

• After acquiring Better Gadgets Inc., Great Widgets Inc. immediately retired all of Better Gadgets Inc.’s debt

a. (5 points) What is the product division’s current WACC? (If you need to make assumptions, state the assumptions clearly and briefly justify when applicable.) [Hint: Apply the WACC adjustment method]

Apply the WACC adjustment method and assume continuous rebalancing

Historical Beta_dP = 0 because r_d = rf = 4%

1. Unlevering formula: Betaap = ![]() Betadp +

Betadp + ![]() Betaep =

Betaep = ![]() 0 +

0 + ![]() 1 =

1 = ![]()

2. Relevering formula: Betaep = Betaap + (Betaap − Betadp) ![]() =

= ![]() +

+ ![]() 04 0 =

04 0 =

![]() 1

1

2

3. r_eP = rf + Beta_eP x MRP = 0.04 + (1/2) x 0.08 = 0.08

4. WACC = (E/V) x r_eP + (D/V) x r_dP x (1 – tax rate) = 1 x 0.08 + 0 = 0.08

b. (3 points) Based on your answer from part (a), what is the NPV of the product division? (If you need to make assumptions, state the assumptions clearly and briefly justify when applicable.) [Hint: Use perpetuity formula]

NPV = 100000/(0.08-0.02) = 1,666,666.67

c. (2 points) What is the NPV of the projected free cash flows from the service division? [Hint: Total firm value = NPV of product division + NPV of service division]

NPV = 1,666,666.67 x 2 = 3,333,333.33

d. (2 points) Based on your answer from part (c), what is the service division’s

current cost of equity? (If you need to make assumptions, state the assumptions clearly and briefly justify when applicable.)

3,333,333.33 = 500000/WACC à WACC = 0.15 = r_e

7. (16 points) Steady Widgets Inc. is a manufacturer of widgets. The company pursues a conservative leverage policy (D/E=0), which has attracted the attention of another firm, Acquisition Company.

Acquisition Company believes Steady Widgets Inc.’s stable cash flows can allow the widget manufacturer to pursue a more aggressive leverage policy and take advantage of tax shields generated by interest expenses. Acquisition Company proposes a “Recapitalization plan”, which is to acquire Steady Widgets Inc. and immediately increase Steady Widgets Inc.’s D/E ratio to 1 (assuming periodic rebalancing). Assume the cost of debt is 10% under the recapitalization plan.

In response to Acquisition Company’s proposal, the current management of Steady Widgets Inc. is contemplating a LBO, in which it will acquire the firm with a mix of debt and equity financing (“LBO plan”). Under the LBO plan, the expected return on debt is 12% during the first two years. Moreover, the firm will also be sold and debt repaid after 2 years (t=2), and it is anticipated the new owners will then immediately adjust the amount of debt to match a target D/V of 0.5 (assuming periodic rebalancing). With the D/V ratio of 0.5, Steady Widgets Inc.’s expected return on debt will be 10%.

For simplicity, assume Steady Widgets Inc.’s company cost of capital is always 13%. Further, assume that Steady Widgets Inc. generates enough pre-tax cash flows such that the full interest expenses can be used to generate tax shields. The corporate tax rate is 25%. Use the information to answer the questions below and express all values in billions of dollars.

The total expected interest expenses and expected FCFs (in billions) for Steady Widgets Inc. over the next two years are given in the table below.

|

|

Year 1 |

Year 2 |

Year 3 and onwards |

|

Total interest expense with LBO |

2.1 |

2.0 |

0 |

|

Total FCF under LBO/Recapitalization plan |

3.0 |

2.5 |

1 |

*FCFs after year 2 are a constant $1 billion per year in perpetuity

a. (3 points) What is unlevered firm value of Steady Widgets Inc. under the LBO plan, but before any transactions are completed? (If you need to make

assumptions, state the assumptions clearly and briefly justify when applicable.)

V_u = 3.0/1.13 + 2.5/1.13^2 + (1/0.13)/1.13^2 = 10.64

b. (2 points) What is the Miles-Ezzell WACC of Steady Widgets Inc. under the

recapitalization plan? (If you need to make assumptions, state the assumptions clearly and briefly justify when applicable.)

WACC_ME = r_a – D/V x r_d x tax rate x (1+r_a)/(1+r_d) = 0.13 – 0.5 x 0.1 x 0.25 x 1.13/1.1 = 0.12 or 11.72%

c. (3 points) Using your calculations in part (b), what is the firm value of Steady

Widgets Inc. under the recapitalization plan, but before any transactions are

completed? (If you need to make assumptions, state the assumptions clearly and briefly justify when applicable.)

V_recap = 3.0/1.12 + 2.5/1.12^2 + (1/0.12)/1.12^2 = 11.31

V_recap = 3.0/1.1172 + 2.5/1. 1172^2 + (1/0.1172)/1. 1172^2 = 11.52

d. (2 points) Under the LBO plan, but before any transactions are completed, what is the interest tax shield in year 1 and the interest tax shield in year 2?

Interest tax shield year 1 = 2.1 x tax rate = 2.1 x 0.25 = 0.53

Interest tax shield year 2 = 2.0 x tax rate = 2.0 x 0.25 = 0.5

e. (2 points) Using your answer in part (d), what is the present value of interest tax

shields for years 1-2 under the LBO plan? (If you need to make assumptions, state the assumptions clearly and briefly justify when applicable.)

Discount using r_d = 12%, which assumes that the debt service is fixed and independent of annual free cash flows generated by Steady Widgets Inc.

PV_ts,1-2 = 0.53/1.12 + 0.5/1.12^2 = 0.87

f. (2 points) Under the LBO plan, but before any transactions are completed, what is the present value of the interest tax shields after year 2? (If you need to make

assumptions, state the assumptions clearly and briefly justify when applicable.)

TV_ts,2+ = TV_L – TV_U = 1/0.12 – 1/0.13 = 0.64

Discount using company cost of capital by arguing that the level of debt after year 2 will be adjusted to a fixed fraction of the future value of assets, implying that the terminal value of tax shields also inherits the risk of the assets.

PV_ts,2+ = 0.64/1.13^2 = 0.50

g. (2 points) Based on your answers in prior questions, what is the total firm value of Steady Widgets Inc. under the LBO plan, but before any transactions are completed? (If you need to make assumptions, state the assumptions clearly and briefly justify when applicable.)

V_LBO = V_u + PV_ts,1-2 + PV_ts,2+ = 10.64 + 0.87 + 0.50 = 12.01

2023-12-19