Coursework of MATH3/69511 Actuarial Models 2023

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Coursework of MATH3/69511 Actuarial Models 2023

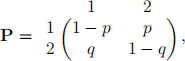

1. For modelling the status of a bank, consider a discrete time, time homogeneous Markov chain with states 1:operating normally, 2:in distress and transition matrix

where q, p ∈ (0, 1) and one time step stands for one year.

(a) (2 marks) Let p = 0.05 and q = 0.75. Given that a bank is currently operating normally, determine the probability that it is operating normally two years later and distressed in the year after that.

(b) (1 mark) Does this Markov chain have a limiting distribution? Explain your answer.

(c) (3 marks) Consider a bank which has to be bailed out for ten billion pounds by the government for each year that it is in distress. It is estimated that the probabilities p and q appearing in the transition matrix are equal to 0.2 and 0.7, respectively, for this bank. Now, in addition to the bail-outs, the government is considering supporting the bank for each year that it is operating normally by an amount of 1 billion pounds because it is expected that then the probability p decreases from 0.2 to 0.1. By looking at the expected costs per year in the long run, should the government introduce this support scheme?

2. Elizabeth has, on each day, the opportunity to do an activity, namely in the evening after work. Each time, she will choose between four activities: going for a walk, watching TV, playing a game or reading a book. When choosing an activity, she uses the following rules:

❼ If it rains outside, she will not take a walk.

❼ If there is nothing good on TV, she will not watch TV.

❼ She will not choose the same activity in two consecutive days.

❼ If multiple options remain, she will decide uniformly at random (i.e. with equal probability), and independently of everything else, which activity (out of the remaining options) to do.

Assume that the probability of rain in the evening of any particular day is 0.3 and is independent of everything else. Also, assume that the event of finding something good on TV has a probability of 0.75 and is independent of everything else.

(a) (3 marks) Let, for n ≥ 1, Xn indicate the activity Elizabeth chooses on the day n. By specifying a state space and the one-step transition probabilities, show that X = {Xn : n ≥ 1} can be modelled as a discrete time Markov chain. Explain how you got your answer.

(b) (2 marks) Given that Elizabeth plays a game on Monday evening, determine the probability that she also plays a game on Wednesday and Friday evening.

3. The following four state Markov jump process with constant transition rates represents a model for the progress of a disease. The transition rates α, β and γ are strictly positive.

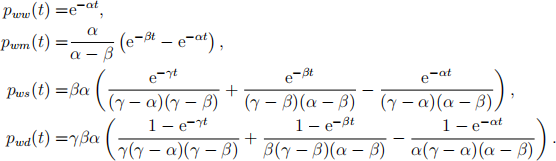

Denote by pij(t) the transition probability from state i to state j over the length of time t, where time is measured in years.

(a) (3 marks) Assume α ≠ β, α ≠ γ and β ≠ γ. Prove the following expressions for pww(t), pwm(t), pws(t) and pwd(t):

(b) (2 marks) Assume a person is currently in the severe stage of the disease. What is the proba-bility that they will remain alive five years later? Explain your answer.

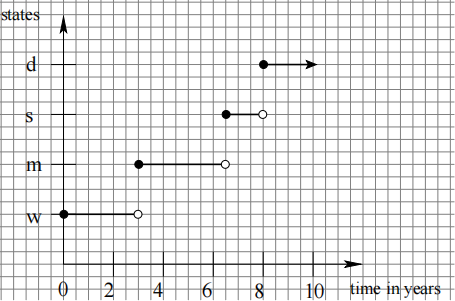

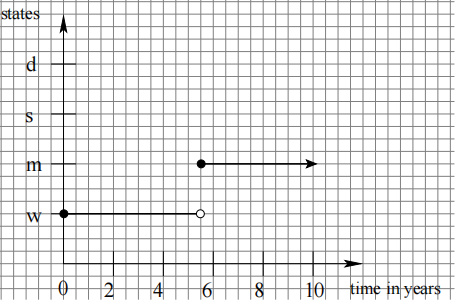

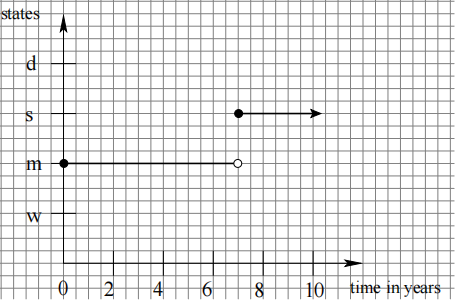

(c) The progress of the disease for three independent patients was observed for ten years in total, and the result of the observations is displayed in Figure 1 for patient 1, Figure 2 for patient 2 and Figure 3 for patient 3.

(i) (1 mark) Derive the maximum likelihood estimates ˆα, βˆ and ˆγ of respectively α, β and γ based on the observations of all three patients.

(ii) (3 marks) Carry out the likelihood ratio test to test, at a 5% significance level, if the transition rate from well to mild is the same as the transition rate from severe to dead. Report your conclusions.

Figure 1: Figure corresponding to Question 1(c).

Figure 2: Figure corresponding to Question 1(c).

Figure 3: Figure corresponding to Question 1(c).

2023-11-30