ECOS3029 Assignment 2

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECOS3029 Assignment 2. Marked out of 35 points.

1. The Monetary Approach to Exchange Rate (12 points in total. 2 points for each question) At time t = 0, the initial log values of the variables L, Y, and M are:

Table 1

What’s more, the continuous growth rate of real income gt and of the money supply μt are:

Table 2

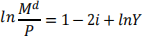

Assume that households care about the opportunity cost of holding money, so that the demand for real money balances in both the U.S.A. and Australia is now given by:

Where i = ln (1 + i) is the log nominal interest rate. Prices are still fully flexible. For the values of Y, M, gt, and μtin Tables 1 and 2, calculate:

a) The nominal interest rate in Australia and the U.S.A. (in log terms) if the log world real interest rate ln(1 + r*) = 0.02 and real interest parity holds.

b) The equilibrium natural log price levels lnp in Australia and the U.S.A. fort = 0;

c) The equilibrium natural log price levels lnp in Australia and the U.S.A. fort = 1;

d) The log of the equilibrium exchange rate lnSt,AUD/USD fort = 0; and

e) The log of the equilibrium exchange rate lnSt,AUD/USD fort = 1.

f) The equilibrium natural log real money balances ln  in Australia and the U.S.A. fort = 0;

in Australia and the U.S.A. fort = 0;

2. (13 points) Now assume that commencing at time t = 1, the Australian central bank

announces an immediate increase to the (continuous) growth rate of the money supply, so

that μt = 0.2 inAustralia. Prices are fully flexible. Draw four graphs (including numerical values on axes) covering the period t = 0 throught = 2 that show:

a) (2 points) The Australian log money supply, lnM; and

b) (3 points) Australian log real money balances and nominal interest rate; and

c) (2 points) The Australian log price level; and

d) (2 points) The log exchange rate lnSt,AUD/USD.

e) (4 points) Write an intuitive explanation for why there is a discrete jumpin several of these graphs.

3. Exchange Rate Parity Conditions (10 points in total. 2 points for each question.)

a) The current value of the spot exchange rate SAUD_CNY = 0.2028. If the Chinese inflation rate for the coming year will be 3% while the Australian inflation rate will be 6%, what value of the exchange rate SAUD_CNY 1 year from now would maintain Relative PPP?

b) Forward Premium. If FUSD_CAD = 1.733 and SUSD_CAD = 1.785 then calculate the forward premium.

c) Assume that (i) one-year forward exchange rate FUSD_GBP = 1.523; (ii) the current spot exchange rate SUSD_GBP = 1.575; and (iii) the one-year interest rate for GBP is 4.665%. What must one-year USD interest rates be for Covered Interest Parity (CIP) to hold?

d) Assume that (i) the current spot exchange rateSDKK/AUD = 5.0183; (ii) the one-

year interest rate for DKK is 3.8%; and (iii) the one-year interest rate for AUD is

2.5%. What must the current expected value of the future DKK/AUD spot exchange rate Et (St+1,DKK/AUD) be for Uncovered Interest Parity (UIP) to hold?

e) Assume that consumers consume only 2 items: Clothing; Food. In New Zealand, clothing for 1 year is NZD 20,000 and food for 1 year is NZD 15,000. In Australia, clothing for 1 year is AUD 40,000 and food for 1 year is AUD 15,000. If the spot exchange rate is SAUD/NZD = 1.616, what is the real exchange rate between

Australia and New Zealand (treat Australia as the domestic country)?

2023-11-02