FINS2624: Portfolio Management 2023 Term 3 Assignment 5

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

FINS2624: Portfolio Management

2023 Term 3

Assignment 5 due Week 7 Tutorial

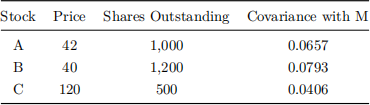

Q1 Assume that the market consisting of only three stocks is in a CAPM equilibrium with a risk free rate of 3%.

(a) Derive the CAPM β of stocks A, B and C.

(b) The expected return on stock B, E[TB ] = 10.93. What are the expected returns on stock A, stock C, and the market portfolio?

(c) Show that the reward-to-risk (using covariance with market as risk) ratios are in parity in a CAPM equilibrium.

(d) Construct a portfolio which has 30% in the risk-free asset and the highest possible Sharpe ratio (i.e. which sits on the Capital Market Line). What would be the portfolio’s expected return E[Tp], standard deviation σp , Sharpe ratio, β, and weighting in each stock?

(e) Plot the Security Market Line, and show where stocks A, B and C sit in relation to it.

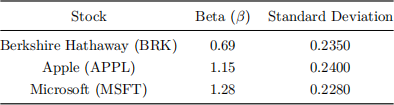

Q2 Assume that three large capitalisation stocks, Berkshire Hathaway, Apple, and Microsoft, have the following risk measures:

The standard deviation of the market portfolio is σM = 15.3%.

(a) Calculate the systematic and unsystematic risk of BRK, APPL and MSFT.

(b) What is BRK’s covariance and correlation with the market portfolio’s return?

(c) Estimate the following covariances: Cov(BRK, APPL), Cov(BRK, MSFT), and Cov(APPL, MSFT). Assume all unsystematic return components are uncorrelated across stocks.

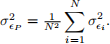

(d) Consider an equally weighted portfolio of BRK and APPL. Calculate the portfolio’s total risk (i.e. variance),

systematic risk and unsystematic risk? Verify that

(e) Consider an equally weighted portfolio of all three stocks. Calculate the portfolio’s total risk (i.e. variance), systematic risk and unsystematic risk? Verify that What happens to unsystematic risk as the number of assets becomes large?

Q3 Consider a market that consists of only two assets, A and B. Asset A has a weight of 0.4 (40%) in the market portfolio and a standard deviation of 0.2 (20%). Asset B has a standard deviation of 0.5 (50%). The correlation between the two assets is 0.3. The expected return on the market is 13%, E[rM ] = 0.13 and the risk free rate is 3%, rf = 0.03.

(a) What is the variance of the market portfolio?

(b) What are the covariances with the market portfolio of the two assets?

(c) What are the CAPM βs of the two assets and the market portfolio?

(d) What are the reward-to-risk (use variance as risk) ratios of the two assets and the market portfolio?

(e) What are the contributions of each asset to the market excess return, E[rM ] − rf?

(f) What are the contributions of each asset to the market variance, σM(2)?

(g) What are the contributions of each asset to the reward-to-risk ratio of the market?

(h) Suppose you had found that the contribution of asset A to reward-to- risk ratio of the market was 1 and that the contribution of asset of B to the same ratio was 0.8. How could you construct a portfolio that beats the market? Could this be an equilibrium?

Selected end-of-chapter questions (optional)

• BKM Chapter 8: Q8,9,10,11,12

• BKM Chapter 9: Q1-4, 9, 17-21

• BKM Chapter 10: Q1,4,5,11

Marking: To obtain the full credit, you need to attempt parts of questions 1, 2, and 3. To obtain half credit, you need to attempt two questions from 1, 2, and 3.

2023-11-01