FINS2624: Portfolio Management 2023 Term 3 Assignment 4

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

FINS2624: Portfolio Management

2023 Term 3

Assignment 4 due Week 5 Tutorial

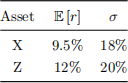

Q1 The risk free rate is 5%. Assets X and Z have expected returns and standard deviations shown in the following table:

(a) What is the Sharpe ratio of each risky asset?

(b) Show how you can dominate asset X using a portfolio that combines asset Z and the risk free asset. (Hint: Find a risky share yZ of Z such that the complete portfolio dominates the expected return-standard deviation of X.)

(c) Show how you can dominate a portfolio with equal weights in asset X and the risk-free asset using a portfolio that combines asset Z and the risk- free asset. (Hint: Find a risky share yZ of Z such that the complete portfolio dominates the expected return-standard deviation of a complete portfolio with risky share yX = 0.5 in X.)

(d) Show (in general) how you can dominate any portfolio combining asset X and the risk-free asset using a portfolio that combines asset Z and the risk- free asset.

Hint: Parts (b) through (d) require you find a dominant portfolio using asset Z. In each case, find a risky share yZ of Z such that the complete portfolio comprised of Z and the risk-free asset dominates a benchmark expected return-standard deviation. That benchmark in (b) is asset X, in (c) is a complete portfolio with yX = 0.5 in X, and in (d) is an arbitrary portfolio with yX > 0 in X. For part (d), find the relationship between yZ of the dominating portfolio and yX of the dominated portfolio

Q2 Suppose that the risk-free rate is 4% and that the corresponding optimal risky portfolio has an expected return of 16% and a standard deviation of 20%. Consider an investor with preferences represented by the utility function U = E [r] − ![]() Aσ 2 , where A = 2.5.

Aσ 2 , where A = 2.5.

(a) What fraction of wealth should they invest in the risky portfolio?

(b) Should they invest more or less in the optimal risky portfolio if they were to become more risk-averse? Why?

(c) Should they invest more or less fraction of her wealth in the optimal risky portfolio if the optimal risky portfolio offers a higher expected return (but the same standard deviation)? Why?

(d) If the risk-free rate were higher than its current 4%, how would you expect the optimal risky portfolio to differ from the current one in terms of expected return and standard deviation?

(e) Now suppose that the investor faces a higher risk-free rate when borrowing (because you are facing more borrowing constraints than the government, or people won’t allow you to borrow at the same rate as the government). Specifically, the investor may lend at a risk-free rate of 4% but has to borrow at a risk-free rate of 5%. Assume for simplicity that the optimal risky portfolio is the same for either 4% risk-free rate or 5% risk-free rate, i.e., with an expected return of 16% and a standard deviation of 20% (this should not be the case in reality, as you will find out in question (d)). What fraction of her wealth should the investor now put in the risky portfolio?

(f) What is the expected return and standard deviation of the portfolio that you found in (e)?

Hint: In part (e), the 4% lending risk-free rate implies a fraction y4 of wealth invested in the optimal risky portfolio. The borrowing risk-free rate of 5% implies a different fraction y5 of wealth invested in the optimal risky portfolio. Determine which is appropriate for the investor given their risk aversion.

Q3 The optimal risky portfolio P* has an expected return of 12.5% and a standard deviation of 25%. The current risk-free rate in the market is 2.0%. Suppose that separation theorem holds, and all investors invest along a common capital allocation line. Consider two different investors. Aggressive investor A holds an optimal complete portfolio which has a standard deviation of 28%. Conservative investor C holds an optimal complete portfolio with a standard deviation of 15%.

a. Draw the capital allocation line. What is the slope of this line and what does it represent?

b. What is the Sharpe Ratio of Investor A and Investor C’s optimal complete portfolio?

c. What is the expected return of Investor A and Investor C’s optimal complete portfolio?

d. What is the allocation to risky assets y* for Investor A and Investor C’s optimal complete portfolio?

e. Derive the implied risk aversion coefficients for Investor A and Investor C.

Marking: To obtain the full credit, you need to attempt all questions except for parts (e) and (f) of Q2. To obtain half credit, you need to attempt Q3 and either Q1 (all parts) or Q2 (parts (a) through (d)).

2023-11-01