FINS2624: Portfolio Management 2023 Term 3 Assignment 3

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

FINS2624: Portfolio Management

2023 Term 3

Assignment 3 due Week 4 Tutorial

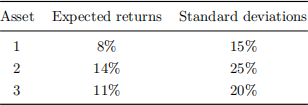

Q1 Consider an investment universe consisting of three assets with the following characteristics:

The correlations between the assets are ρ1 ,2 = 0.5, ρ2 ,3 = 0.35, and ρ1 ,3 = 0.25.

a. What is the expected return and standard deviation of an equally weighted portfolio invested in all three assets (ω = 1/3 for all assets)?

b. What is the diversification benefit for an investor that switches her investment to the equally weighted portfolio from an investment consisting only of asset 3?

c. When choosing between investing all her capital in asset 2 or in the equally weighted portfolio, what would an investor with quadratic utility and a risk aversion parameter A = 3 choose?

d. What about an investor with quadratic utility and a risk aversion parameter A = 1?

e. What is the covariance between the return on the equally weighted portfolio invested in all three assets and the return of an equally weighted portfolio invested only in assets 1 and 3?

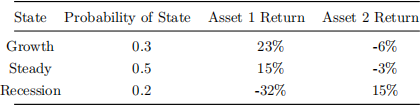

Q2 Consider two assets which are negatively correlated. Suppose the distribution of return scenarios for these assets in different probability weighted future scenarios is given by:

a. What are the expected returns and standard deviations of Assets 1 and 2? What is the covariance and

the correlation between Asset 1 and Asset 2?

b. We want to construct a portfolio weighted 70% in Asset 1 and 30% in Asset 2. What is the portfolio expected return and standard deviation?

![]()

![]()

![]() Q3 Suppose all investors have preference described by the quadratic utility function with A > 0:

Q3 Suppose all investors have preference described by the quadratic utility function with A > 0:

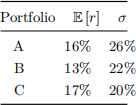

Each investor has to choose between three portfolios with the following characteristics:

a. Which portfolio would every investor pick and why?

b. What utility would an investor with a risk aversion coefficient A=2 get from the three portfolios?

c. What is the risk aversion coefficient of an investor that is indifferent between portfolio A and portfolio B?

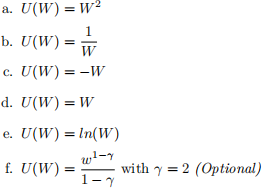

Q4 Consider the following utility functions, where W is wealth:

How reasonable are each of these functions in representing actual investor preferences? Why?

Marking: To obtain the full credit, you need to attempt all questions except for Q4, part f. To obtain half credit, you need to attempt three of the four questions.

2023-10-31