FINS2624: Portfolio Management 2023 Term 3 Assignment 2

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

FINS2624: Portfolio Management

2023 Term 3

Assignment 2 due Week 3 Tutorial

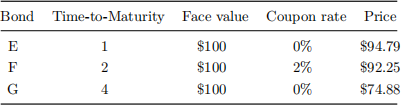

Q1 Suppose the following bonds are trading in the market.

In addition to the bonds above, you also observe the 1-year forward rate in 2 year’s time, 2 f3 is 8.50%. You wish to price Bond H, which is 4-year 10% coupon bond with a face value of $100. Assume all bonds (and the forward rate) are risk-free and that Bond F and Bond H are annual coupon bonds.

a. Infer the term structure of interest rates: y1, y2, y3 and y4. These are the yield on the pure yield curve for years 1-4.

b. Price Bond H using the pure yield curve.

c. Based on the pure yield curve, infer the 2-year forward rate commencing in 2 year’s time 2 f4 .

d. Assume Liquidity Preference Theory holds and the annual liquidity premium is flat at 1.00% for all t. What is the expected future 1-year spot rate in 3 year’s time E [3 y4]?

e. Assume the Expectations Hypothesis holds. What is the expected 1-year future spot rate in 1 year’s time E [1 y2]?

Q2 Consider a four-year bond with a face value of $100 and a coupon rate of 10%. The term structure of interest rates is flat at 5% (i.e. yt = 5% for all t).

a. Calculate the duration of this bond, and use the duration rule to estimate the dollar change in price if the term structure of interest shifts to 6%?

b. What would the actual price change be?

c. Explain the approximation error that arises from using duration rule by comparing the linear rule to the actual price-yield relationship. What it the relationship between yield and duration?

d. Assume yields instead shift rom 5% to 4%? Is the magnitude of the price change larger or smaller compared to the shift from 5% to 6% in part a? Explain why this occurs.

Q3 In this problem, the term structure of interest rates is flat at 8%. The following bonds and liabilities are given:

• Bond A: A zero-coupon bond with a face value of $100 and a time to maturity of 2 years.

• Bond B: A zero-coupon bond with a face value of $100 and a time to maturity of 6 years.

• Bond C: A zero-coupon bond with a face value of $100 and a time to maturity of 9 years.

• Liability X: A one-time liability of $100 maturing in 3 years.

• Liability Y: A one-time liability of $100 maturing in 7 years.

a. Suppose you have liability X and want to immunize it using bonds A and B. What should you invest in each bond?

b. Suppose you have liability X and want to immunize it using bonds B and C. What should you invest in each bond?

c. Suppose you have both liabilities X and Y and want to immunize your position using bonds B and C. What should you invest in each bond?

Q4 Consider the following bonds:

• Bond A: A 2-year zero-coupon bond with a face value of $100 and 6% YTM.

• Bond B: A 2-year par-value bond with a face value of $100 and 6% coupon.

• Bond C: A 2-year par-value bond with a face value of $100 and 7% coupon.

• Bond D: A 3-year par-value bond with a face value of $100 and 7% coupon.

• Bond E: A 4-year par-value bond with a face value of $100 and 7% coupon.

• Bond F: A 4-year discount bond with a face value of $100 and 7% coupon.

If the yields off all bonds increase by one percent,

a. Which bond among bonds A, B and C will experience the largest percentage price change? Which will have the lowest percentage price change?

b. Which bond among bonds C and D will experience a larger percentage price change?

c. Would you expect the difference in percentage price change to be bigger between bonds C and D or between bonds D and E?

d. Which bond of bonds E and F will experience a larger percentage price change?

Hints: Recall that a par-value bond is a bond trading at its face value. This occurs when the yield on the bond is equal to its coupon rate. If you have not yet developed intuition for these questions, build a spreadsheet that prices the bonds at the current yields and then after a one percent change. Then, try to reason through the questions logically with the results known.

Marking: To obtain the full credit, you need to attempt all questions. To obtain half credit, you need to attempt three of the four questions.

2023-10-30