FINC6010 – Derivative Securities Assignment – 2023 Semester 2

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Discipline of Finance

FINC6010 – Derivative Securities

Assignment – 2023 Semester 2

1. Due date and time: 18 October 2023 by 23:59.

2. Please include a cover sheet containing your group name and the student number of each group

member. Cover sheet does not contribute to the total number of pages for the assignment.

3. Assignments must be typed and submitted via Turnitin through Canvas.

4. Maximum length is 12 pages with font size 11pt or larger. Cover sheet and references (if any) do not contribute to the assignment length.

5. This is not intended to be a formal report, so please do not write background information, definitions presented in lectures, and other facts not explicitly required in answering the ques- tions.

6. Please keep your answers as brief as possible and only write information explicitly relevant to the questions asked. Marks will not be awarded to (parts of) answers not explicitly relevant to the questions asked nor will marks awarded based on the lengths of the answers.

7. Penalty of 5% per calendar day, or part thereof, will apply to late submissions.

8. Do not attach printouts of Excel spreadsheet to the assignment.

Background Information on RMBS

The purpose of this assignment is to introduce you to residential mortgage backed securities (RMBS) that are derivatives on a pool of mortgages. Although we do not directly cover these in this unit, the same principles introduced in lectures apply to computing their values and assessing the risks. Given below are some basic background information on RMBS:

– Financial institutions (FI) that offer residential mortgages often raise funds on the short term market and lend those funds out in long term mortgages.

– When the total (principal) value of mortgages becomes large, FIs “package” the loans into an RMBS and sell these products to investors.

– Investors in RMBS invest a lump sum amount upfront and receive payments (coupons) over time that come from the underlying mortgages in the form of of interest and principal repay- ments. Provided there are no defaults on the underlying mortgages, investors will receive back their initial investment along with interest payments over time.

Discount Factors, Log-linear Interpolation, and Parallel Shift

The concept of time value of money implies that $1 at some future time T is worth less in today’s terms. The purpose of discount factors, γ(T), is to capture the time value of money as a function of time T.

In practice, discount factors are inferred from market quoted rates, and since there are only finitely many such quoted rates, discount factors are determined for only a finite number of maturities,

say T1 < T2 < · · · < Tn. Since we will need discount factors for other maturities to value financial assets in general, we need a way of “interpolating” these discount factors. In this assignment we will use log-linear interpolation of discount factors.

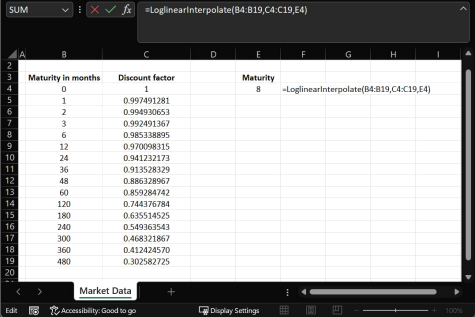

Spreadsheet, FINC6010_assignment_2023_s2.xlsm, is available from Canvas and contains the func- tion LoglinearInterpolate for performing the required interpolation. The spreadsheet also contains the discount factors needed to answer the assignment questions. When you open the spreadsheet for the first time, you will be asked if you trust the source and whether or not to enable macros. Please respond “yes” to both. The function LogLinearInterpolate takes as input a vertical array of “x” values, a vertical array of corresponding “y” values, and finally the point at which you need the interpolated value as shown in Figure 1.

Figure 1. Log-linear interpolation function.

If your PC does not allow you to download the spreadsheet FINC6010_assignment_2023_s2.xlsm, then you can create an Excel spreadsheet with the required interpolation function as follows:

A. Download from Canvas the spreadsheet named FINC6010_assignment_data_2023_s2.xlsx con- taining the discount factors, and the file named LoglinearInterpolate.bas.

B. Open FINC6010_assignment_data_2023_s2.xlsx and (re)save with a name of your choice but with file type Excel Macro-Enabled Workbook (*.xlsm).

C. Open a VBA code editor by hitting ALT and F11 simultaneously.

D. From the left panel of VBA editor, right click on your VBA project, then Import File. . . to launch an OpenFile dialogbox.

E. Locate the file LoglinearInterpolate.bas downloaded from Canvas and click the Open but- ton. You will now have a new function with name LogLinearInterpolate in your Excel spread- sheet.

For the purposes of this assignment, parallel shift of an interest rate curve by δ (for example, δ = 0.0001) will mean changing the given discount factor γ(Ti ) to γ(Ti )e − δTi /12 for 1 ≤ i ≤ n, assuming Ti are measured in months. Note that the sign in the exponent is negative since the parallel shift refers to the shift in interest rates (associated impact on discount factors is in the opposite direction).

Questions

1. A key risk factor for an FI providing mortgages is borrowers defaulting on their loans and the property values not being sufficient to cover the loans. Explain briefly how FI can mitigate this risk. [2 marks]

2. By packaging a set of mortgages into an RMBS and selling the underlying loans to investors, FI gives up the relatively high interest payments it would have earned on the loans. Explain briefly why an FI would offload the loans to RMBS investors and give up the relatively high interest payments? [2 marks]

3. Explain very briefly the risks for an RMBS investor. [2 marks]

4. Given that there are risks associated with an RMBS, why would an investor consider investing in an RMBS. [2 marks]

5. Explain the legal difference between the Australian and the US market that makes mortgages in Australia less risky for the lenders (and RMBS investors) in the event of default. [2 marks]

6. In establishing an RMBS, the legal ownership of the underlying loans are transferred from the FI to a special purposes vehicle (SPV) that is independent of the FI. Moreover, rather than RMBS investors receiving the repayments made on the underlying loans directly, RMBS is usually structured to involve a swap provider who receives the payments from the underlying loans and provides the interest and principal repayments to the investors. [4 marks]

(a) Explain briefly why the legal ownership of the loans underlying an RMBS is transferred to an SPV. [2 marks]

(b) Explain briefly the purpose of the RMBS swap provider that receives repayments on the underlying loans and provides payments to the investors. [2 marks]

7. Swap providers are usually large banks, and they are required by regulations and internal risk policies to hedge risks appropriately. [4 marks]

(a) Give one risk factor for the swap provider that can be hedged. Briefly explain how this risk arises and how it can be hedged. [2 marks]

(b) Give one risk factor for the swap provider that is difficult to hedge. Briefly explain why it is important for this risk to be hedged and why it is difficult to hedge. [2 marks]

8. In marketing an RMBS to investors, ratings agencies are usually engaged to assign a credit rating on the RMBS. One of the conditions that rating agencies impose is that the swap provider must maintain a minimum credit rating. If the swap provider fails to maintain this minimum requirement, then highly unfavourable capital restrictions are imposed on the swap provider. In such cases, the swap provider whose credit rating is downgraded will often “novate” the RMBS swap. That is, they will find another bank that meets the credit rating requirement to replace them as the RMBS swap provider. This is known as swap novation, and involves the original and the replacement RMBS swap providers exchanging the agreed value of the RMSS swap at the time of swap novation. [4 marks]

(a) Explain briefly why rating agencies may be engaged on RMBS issues. [2 marks]

(b) Explain briefly why credit rating agencies require the swap provider to maintain a high credit rating and impose highly unfavourable capital restrictions (such as requiring the swap provider to hold a certain fraction of remaining swap notional in highly liquid assets) when this condition is not met. [2 marks]

9. When an RMBS swap is novated (usually following a credit rating downgrade of a swap provider), the swap is valued favourably to the bank taking over the role of the swap provider (novating bank). That is, the swap is novated at a profit to the novating bank. The trading desk in the novating bank usually tries to claim this profit upfront when the novation takes place. [4 marks]

(a) Explain briefly why the original swap provider would novate the RMBS swap at a value that is unfavourable. [2 marks]

(b) Explain briefly why the management of the novating bank would not allow the trading desk to realize the expected profit from the novated swap upfront. [2 marks]

10. The purpose of this question is to provide you with some insights on how various risk factors affect the net present value of an RMBS. It will be assumed that repayments on the loans underlying the RMBS, including any prepayments, are made at the end of each month. For simplicity, we will make the following assumptions: [10 marks]

– Loans underlying the RMBS are homogeneous so that they all behave the same way.

– Mortgage rate R = 0.5% per month (not annualized) and is fixed. That is, if Pi is the remaining principal at the start of month i, then the remaining principal at the end of the month, ignoring interest repayments and prepayments, is Pi (1 + R).

– Initial remaining loan principal is P1 = $1, 000, 000.

– Regular monthly repayment on the loans is M = $19, 332.80.

– Loans have n = 60 months remaining to maturity.

– Expected prepayment at the end of each month is β = 2% of remaining principal at the start of the month.

– Discount factors are as given in FINC6010_assignment_2023_s2.xlsm.

– If Pi is the remaining principal at the start of month i, then the remaining principal at the end of the month is

Pi+1 = max (Pi (1 + R) − M − βPi , 0) .

– At the end of month i, an RMBS investor receives

Ci = min (Pi (1 + R) , M + βPi ) . (1)

(a) Explain the expression for the payment, Ci , received by the investor at the end of i-th month given in (1). [2 marks]

(b) Compute the net present value (NPV) of the RMBS to the investor. That is, compute

NPV = ![]() γ(Ti )Ci ,

γ(Ti )Ci ,

where Ti is the time to end of month i. Provide the values C5 and γ(T5 ) for the 5-th payment (to nearest cent) and discount factor (to 6 decimal places) used in the calculation. [2 marks]

(c) Compute the NPV of the RMBS as a function of the prepayment rate β and parallel shift to the interest rate curve δ by completing Table 1 below (give NPV to the nearest cent) where p is the number of payments received by investors. Describe and explain the impacts of the prepayment rate, β, and the parallel shift, δ, to the discount curve on the value of the RMBS. [4 marks]

|

(β, δ) p NPV |

|

(10%, 0.000) (10%, 0.001) (30%, 0.000) (30%, 0.001) (50%, 0.000) (50%, 0.001) |

Table 1. Table to complete for Q10 part (c)

(d) Consider the following scenarios: (A) market moving from low interest rate environment to high interest rate environment, (B) steady interest rate environment, and (C) market moving from high interest rate environment to low interest rate environment. Under which of these scenarios would fixed rate RMBS be most attractive to investors? [2 marks]

11. What other assets can FI package into an asset backed security and sell to investors? Briefly explain whether this asset backed security represents higher risk for investors when compared to RMBS. [4 marks]

2023-10-21