FINM7409 Tutorial 2

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

FINM7409

Tutorial 2 Solutions

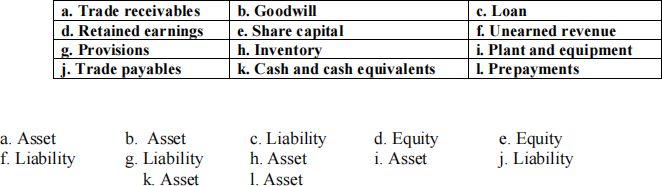

4.16 Classify each of the following according to whether it is an asset, liability or equity account. Apply your learning from the definitions in the introduction to accounting and business decision making chapter to provide a justification for each classification.

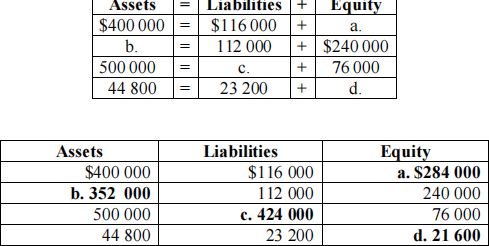

4.17 Using your knowledge of the accounting equation, solve the missing values in the following table:

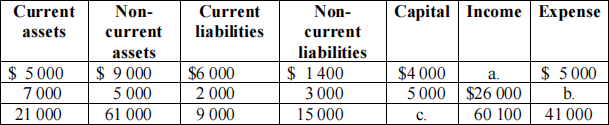

4.18 Determine the missing entries:

a. 7600

b. 24 000

c. 38 900

4.20 State the effect of each of the following business transactions for Tundi's

Trevor. For example, in (a) we increase cash and increase capital.

a. Tundi Trevor commenced business by injecting cash into her business.

b. Paid wages.

c. Purchased goods for sale on credit.

d. Sold goods on credit

e. Received an invoice for annual insurance on building and paid the account.

f. Tundi Trevor withdrew an iPad from the business.

g. Sold inventory for cash.

h. C Ho (accounts receivable) paid amount outstanding.

i. Tundi's Trampolines paid accounts payable in full.

a. increase cash and increase capital

b. decrease cash and decrease profit or loss (equity)

c. increase inventory and increase accounts payable

d. increase accounts receivable and increase profit or loss (equity)

e. decrease cash and decrease profit or loss (equity)

f. decrease office equipment and decrease capital

g. increase cash and increase profit or loss (equity), decrease inventory and decrease profit or loss (equity)

h. decrease accounts receivable and increase cash

i. decrease cash and decrease accounts payable

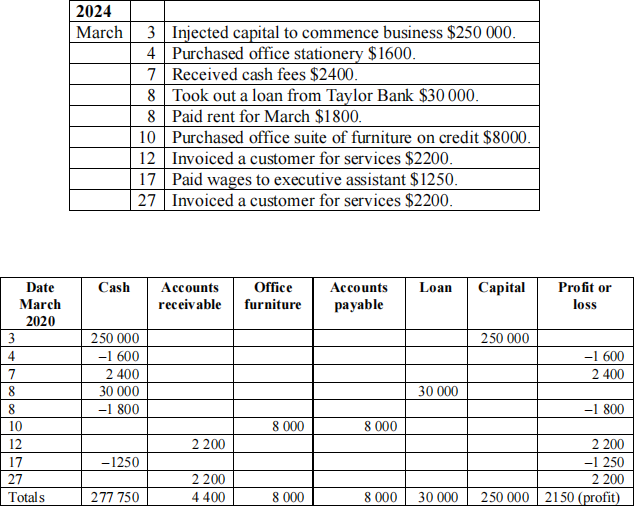

4.26 Preparing a worksheet

Enter the following transactions for the month of March 2024 in a worksheet and calculate the profit or loss for the period. Explain how the worksheet assists in the calculation of profit or loss.

Please note: March 4 could alternatively be recorded as an asset (office stationery). So instead of – 1600 profit or loss it would be + 1600 office stationery (asset). The decision to expense or capitalise office stationery as an asset depends on the size of the business and the frequency of stationery purchases. For example, if the stationery purchase is for a month then it’s more likely to be an expense. If it is purchased in large amounts for the year, then the purchase should be treated as an asset. It is not a credit transaction as, unlike March 10, it does not state ‘on credit’ .

4.27 Preparing a worksheet

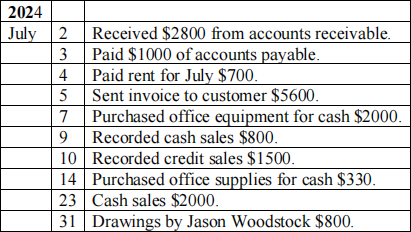

The closing statement of financial position items are given below for Jason Rosco in in accounting equation form as at 30 June 2024. Transactions for the following month of July are also given.

Transactions for July 2024 were as follows:

Required

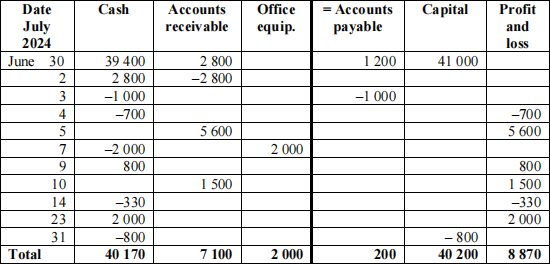

a. Prepare worksheet entries for the business transactions for the month ended 31 July 2024.

b. At the end of July, Jason realised that the customer invoice sent on 5 July was recorded incorrectly. The correct amount should be $6500. Explain what type of error Jason made and explain the impact of this error on the statement of financial position and the statement of profit or loss.

a.

a. This is a transposition error. You can identify it as a transposition error as the difference (6500 and 5600) is divisible by 9.

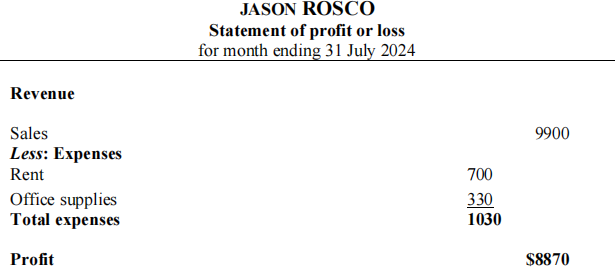

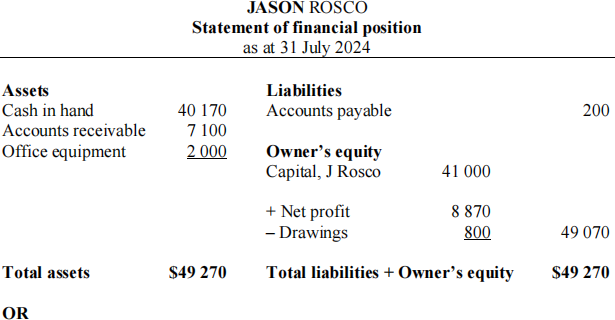

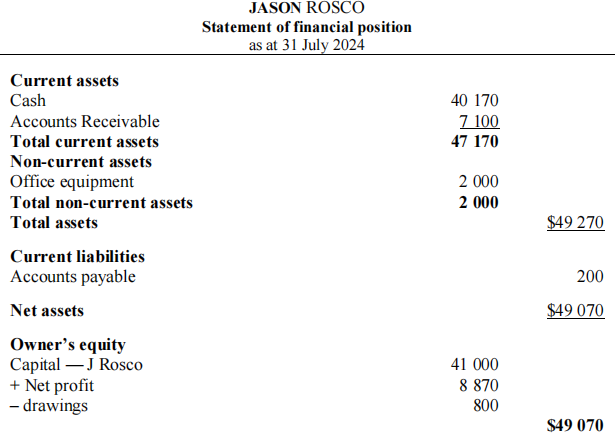

4.28 Preparing statement of profit or loss and statement of financial positions Using the information in 4.27, prepare:

a. a statement of profit or loss for the period ending 31 July 2024 b. a statement of financial position as at 31 July 2024.

a.

b.

4.29 Allocating transactions and demonstrating duality

Choose appropriate account names and demonstrate the dual effect that occurs when the following business transactions for Larry Little take place. For example, in (a) we would increase cash $22 000 and increase capital $22 000.

a. Larry Little commenced business by contributing $22 000 cash.

b. Received 170 000 income for services performed.

c. Paid telephone account $382..

d. Larry Little withdrew cash from business $1600..

e. Purchased office stationery on credit 3800..

f. Cash sales $1400.

g. Credit sales of $$1400.

h. Brett Little withdrew office equipment from business $2000.

i. Brett Little negotiated with possible business partner to contribute $40 000 as a silent partner to the business.

j. Brett Little purchased meal for his partner’s birthday on his personal credit card.

a. Increase cash $22 000 and increase capital $22 000

b. Increase cash $170 000 and increase revenue $170 000

c. Decrease cash account $382.and increase telephone account $382.

d. Decrease cash $1600.and increase drawings $1600.

e. Increase office stationery on credit $3800 and increase accounts payable $3800

f. Increase cash $1400. and increase sales revenue $1400.

g. Increase accounts receivable $1400.and increase sales revenue $$1400.

h. Brett Little (assume he is Larry’s brother or son) Decrease office equipment $4000 and increase drawings $4000

i. No recording necessary as it is not a business transaction

j. Meal was purchased on personal credit card so is not a business transaction.

Instructor’s note: In the solution for 4.29, we have assumed that it is account names not worksheet columns. If it was worksheet columns, then the profit or loss column would be used for all of the revenue and expense transactions.

5.5 The statement of financial position for Daffodil Pty Ltd reveals cash on hand of $8000, accounts receivable of $48 000, inventory measured at $50 000 and plant and equipment measured at $116 000. The liabilities of the entity are: accounts payable $28 000, bank overdraft $32 000 and long- term loan $180 000. Relate this information to the liquidity of the entity.

Liquidity refers to the ability of the entity to pay their debts as they fall due. Liquidity can be assessed by comparing the entity’s current assets and current liabilities. The current assets of Daffodil Pty Ltd total $106 000 being: cash $8000, accounts receivable $48 000 and inventory $50 000. The entity’s current liabilities are $60 000 being the accounts payable $28 000 and bank overdraft of $32 000. As the loan is long-term, it is assumed that the loan is for a period exceeding one year and therefore is not a current asset. As Daffodil Pty Ltd’s current assets exceed their current liabilities, the entity would not appear to have a liquidity problem. This assumes that the inventory is saleable, the cash can be recovered from the debtors and the entity is generating sufficient cash flow to service its debt obligations. Given the entity’s stated liabilities exceed its stated assets, the entity’s equity is negative. This suggests that the entity has accumulated losses.

5.6 An entity has total assets measured at $330 000 on the statement of financial position. The entity’s liabilities total $150 000, of which $90 000 is a bank loan. Calculate the entity’s net assets. Discuss the entity’s financing decision.

Net assets refer to an entity’s total assets less total liabilities. Given that the entity’s assets are $330 000 and the total liabilities are $150 000, the entity’s net assets are:

Net assets = Assets – Liabilities

= $330 000 – $150 000

= $180 000

The entity is financing its assets with $150 000 of liabilities and $180 000 of equity. This means that the entity is using more equity than debt to finance its assets. For every $1 of assets, the entity has $0.45 of liabilities and $0.55 of equity. Relative to equity funding, interest-bearing debt has to be serviced via regular interest payments and the entity would have to have sufficient cash to meet these fixed interest payments.

5.8 The Digital Marketing Company wants to increase its asset base by recognising its customer list as an asset. Discuss whether this is permissible under accounting standards.

Customer lists are regarded as intangible assets and accounting rules applicable from 1 January 2018 to reporting entities under AASB 138 Intangible Assets specify that certain intangible assets (such as brands, mastheads, publishing titles or customer lists) that are internally generated (rather than being purchased) cannot be recorded as assets on the statement of financial position (para. 48). Prior to 1 January 2005, Australian entities had discretion to record such internally generated intangibles as assets. This means that the company would not be able to increase its asset base by recognising its customer list in the statement of financial position.

While it can be argued that such assets satisfy the asset definition criteria, regulators’ concerns are that being able to reliably measure such assets, when they do not trade in an active and liquid market, is problematic. If the company had acquired the customer lists as part of a business acquisition, it could legitimately record them as intangible assets since they had been purchased.

Accounting for intangible assets is controversial and many Australian firms were opposed to being disallowed the opportunity to recognise internally generated intangible assets as assets on the statement of financial position.

Suggestion: show students an extract of a company report with derecognised identifiable intangibles — Coca-Cola would be a good example given that it had to derecognise many millions of dollars of intangible assets. It is interesting to explore students’ views as to the appropriateness of having different accounting treatments for internally generated versus acquired intangible assets.

5.10 Knowing that you have some accounting experience, a friend has sought

your advice regarding a business that she intends purchasing. The statement of financial position for the business shows total assets of $240 000 and liabilities of $120 000. The selling business has provided no notes to accompany the statement of financial position. On the basis of the information provided, your friend believes the business is worth $120 000. Advise your friend as to the accuracy of her assessment and what questions regarding the statement of financial position she should ask the seller of the business.

The carrying amount of the net assets of the entity is $120 000 (i.e. the $240 000 assets less the $120 000 liabilities). However, this does not mean that this is what the net assets of the entity are worth. Considering the variety of measurement bases that can be applied to an entity’s assets and liabilities and the possibility that a business may have valuable resources that are not captured on the statement of financial position (i.e. strong management), a statement of financial position does not portray the worth of the entity. To illustrate, consider an entity that acquired some land at a cost of $200 000 five years ago. The entity can legitimately report the land on the statement of financial position at its historical cost (i.e. $200 000). This will not necessarily bear any resemblance to the current value of the land. Assuming that real estate prices have increased, the land may currently be valued at $500 000. Therefore, carrying it at $200 000 on the statement of financial position is not reflecting its current value. As the statement of financial position does not reflect the current value for all assets and liabilities, valuing an entity based on the carrying amount of the net assets may be inappropriate. Usually, it would be expected that the entity is worth more than the net assets reported on the statement of financial position.

This question highlights the importance of ascertaining things such as:

. the measurement bases applied to the various asset and liability classes

. the depreciation method and assumptions used to calculate depreciation

. the amount of inventory on hand

. the age of the debtors

. the underlying profitability of the business

. the cash generating capability of the business

. an independent valuation of assets such as property, plant and equipment.

5.11 As an investor in equities, you use the financial statements to assess the

financial condition of entities and inform your investment decisions. Discuss if you would find it more useful to have items of PPE valued at historical cost or fair value.

An investor requires information that is both relevant and reliable for their decision making. Often it is necessary to trade-off the desirable characteristics of relevance and reliability. This is evident when considering historical cost and fair value. Generally, the fair value of property, plant and equipment (PPE) is more relevant to assess the financial position of the entity relative to historical cost. Fair value is the price at which a willing, knowledgeable seller and buyer would exchange an asset in an arms’ length transaction. Knowing the fair value of the PPE gives the investor a better indication as to what the assets are worth in the market. However, without a sale transaction to verify the fair value, subjectivity is introduced into the measurement process. Thus, compared to historical cost that is more objective, fair value may not be as reliable.

To extend this question, other issues that could be raised include:

. the importance of recognition relative to disclosure

. if items of PPE are measured at historical cost, would investors find it useful to have the fair values disclosed?

. how could the investors assess the reliability of the fair value?

5.13 Kookaburra Ltd is always running short of cash, despite growing sales

volumes and its current assets exceeding its current liabilities. A review of its operations by a consultant finds that a considerable portion of the company’s inventory is obsolete stock for which there is limited demand. Further, many of the accounts receivable are overdue by more than 60 days. The accounts receivable and inventory are carried at their gross amount and cost value, respectively, on the statement of financial position. Explain how the accounts receivable and inventory should be valued on the statement of financial position. If Kookaburra Ltd was to apply the correct measurement basis, determine the effect on: (1) profit; and (2) assets.

Accounts receivable should be measured at their cash equivalent. This is the cash that the entity expects to recover. The carrying amount assigned to accounts receivable should reflect the monies owed to the entity less an allowance for doubtful debts. The allowance for doubtful debts represents the entity’s estimate of the monies not expected to be received. When estimating the amount to record as the allowance for doubtful debts, entities consider the time for which the debt has been outstanding (e.g. the collectability of debts related to invoices from 6 months ago may be remote if the monies were due one month from the invoice date). Alternatively, based on past experience, the entity may provide for a certain percentage of the current period’s sales to be treated as doubtful.

Inventory must be measured on the statement of financial position at the lower of cost and net realisable value. Net realisable value is the amount that the inventory could be sold for in an orderly fashion less estimated selling costs. Thus it is necessary to compare the cost price of inventory with the net realisable value with the lower valuation assigned to the inventory for statement of financial position purposes. For example, if inventory has a cost price of $20 000 and it has a net realisable value of $30 000 the value assigned to the inventory in the statement of financial position would be $20 000 as the cost is lower than the net realisable value. Conversely, if inventory has a cost price of $20 000 and it has a net realisable value of $15 000 the value assigned to the inventory in the statement of financial position has to be $15 000 as the net realisable value is the lower value. In the latter case, this would mean that the inventory, currently recorded at its cost price of $20 000, would have to be written down by $5000 to $15 000. Given that an asset has been reduced, to keep the statement of financial position equation in balance, an expense of $5000 is recorded in the statement of profit or loss being the inventory write-down. Students will explore the concept of income and expenses in chapter 6.

If Kookaburra Ltd was to apply the correct measurement basis for its accounts receivable, the entity firstly would need to estimate how much of its accounts receivable would be uncollectable, since many of its accounts receivable are already overdue. The estimated uncollectable accounts receivable is then debited as a bad debt expense and is recognised in the statement of profit or loss, which subsequently would reduce the entity’s profit in the current accounting period. At the same time, the estimated uncollectable accounts receivable is also credited to an allowance for doubtful debts account, which is a contra asset account that reduces the amount of accounts receivable. As a result, applying the correct measurement basis for accounts receivable will reduce Kookaburra Ltd’s profit for the current period and its assets.

Similarly, if Kookaburra Ltd was to apply the correct measurement basis for its inventory, the inventory must be valued at the lower of cost and net realisable value. As a considerable portion of Kookaburra Ltd’s inventory is already obsolete, the inventory must be written down to net realisable value. The inventory write-down will reduce the inventory value recognised in the statement of financial position, and will be treated as an expense in the statement of profit or loss. As a result, Kookaburra Ltd’s profit in the current period and its assets will also decrease.

5.20 Solve for the missing financial numbers as they would appear on the statement of financial position.

|

a. 81 000 (35 000 + 46 000) b. 9 000 (37 000 – 28 000) c. 14 000 (44 000 – 30 000) d. 57 000 (81 000 + 60 000 – 84 000) e. 141 000 (81 000 + 60 000) f. 52 000 (81 000 – 29 000) g. 136 000 (295 000 – 159 000) h. 122 000 (295 000 – 157 000 – 16 000) |

i. 138 000 (122 000 + 16 000) j. 15 900 (22 900 + 17 000 – 24 000) k. 39 900 (15 900 + 24 000) l. 14 800 (17 000 - 2200) m. 82 186 (129 127 – 46 941) n. 28 255 (68 755 – 40 500) o. 11 622 (60 372 – 48 750) |

5.21 Identify whether the following assets would be classified as current or non-

current as at the end of the reporting period and justify your classification decision.

a. Right-to-use assets

b. Intangible assets

c. Property

d. Accounts receivable

e. Deferred tax assets

f. Inventory

The distinction between current and non-current assets is normally based on when the future economic benefit is expected to occur. If within 12 months (i.e. the next reporting period), the item is classified as current; if beyond 12 months, the item is classified as non-current.

a. Right-to-use assets arise through contracts that give the entity (the lessee) the right to use the asset for a certain period of time in exchange for consideration (such as leases). The classification as current or non-current will depend on the term of the right to use the asset.

b. Intangible assets are non-current assets as it is expected to generate economic benefits over a period greater than 12 months.

c. Non-current asset, as the benefits of using property are expected to occur beyond 12-month period.

d. Current asset, as the amount owing by the debtors are expected to be received within 12 months.

e. Deferred tax assets are a non-current assets as the benefit from the temporary tax difference is likely to be greater than 12 months.

f. Inventory would be classified as current assets as they are available for sale and would be expected to be sold within the next 12 months.

5.22 Identify whether the following liabilities would be classified as current or

non-current as at the end of the reporting period and justify your classification decision.

a. Provision for employee long service leave

b. Long-term bank loan

c. Lease liabilities

2023-08-31

Financial Mangement for Decision Markets