ECO00056M Fixed Income Securities MSc Degree Examinations 2018

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECO00056M

MSc Degree Examinations 2018

DEPARTMENT OF ECONOMlCS & RELATED STUDlES

Fixed Income Securities

Time Allowed: TWO hours

Answer any THREE questions

1. Assume that today is 15 February 2018. You observe the following bond prices:

(a) [10 marks] From the observed bond prices compute the continuously compounded yield curve.

(b) [8 marks] using the information found in (a), calculate the price of the

2.5-year loating rate bond with 50 basis point spread with annual

payments. You know that at the last coupon payment date, 6 months ago, the annually compounded rate was 2.1%.

(c) [7 marks] A trader is conident that interest rates will increase in the next

few days and would like to execute a speculative, self-inancing trade based on her belief. sketch a scheme of a reverse repo transaction with the repo dealer that will allow you to sell the bond at time t and buy it at time t 十 n. what are the cash lows at these dates?what will be the trader,s proit on this transaction?

2. The current, semi-annually compounded yield curve is as in the following table:

(a) [10 marks] compute the duration and dollar duration of the portfolio consisting of the following securities:

. 3-year zero coupon bond

. 1-year coupon bond paying 4% semiannually

. 2-year loating rate bond with a 40 basis point spread, paid semiannually.

(b) [8 marks] Find and interpret the duration based monthly 95% value-at-Risk of the portfolio from (a). Assume that the monthly changes in the level of interest rates are normally distributed as dT 个 N (0, σ2 ), where σ = 0.4%. [Note: The 5一th percentile of the standard normal distribution is equal to 一1.645.]

(c) [7 marks] Find and interpret the duration based monthly 95% Expected

shortfall of the portfolio from (a). Assume that the monthly changes in the level of interest rates are normally distributed as dT 个 N (0, σ2 ), where

σ = 0.4%. [Note: The 5 一 th percentile standard normal probability density and cumulative distribution function amount to 0.1031 and 0.0500,

respectively.]

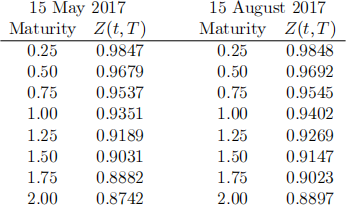

3. use the data in the table to answer the following questions.

(a) [10 marks] on 15 May 2017 a company is interested in purchasing $50

million worth of 1 1/2一year zero coupon Treasuries with the proceeds of a sale of equipment to take place in 6 months (i.e. the maturity of the

Treasuries is 15 May 2019). The company is interested in locking in the price of the Treasuries today through a forward contract. what would the forward price be of the Treasuries?How many bonds will the company purchase?

(b) [8 marks] Three months have passed, so that today is 15 August 2017 (see the right panel of the table). what is the value of being long the forward contract from (a)?lf the company decides to close this contract, would it make money or lose money?

(c) [7 marks] what are the advantages and disadvantages of hedging the interest rate risk with options versus futures?

4.

(a) [10 marks] A homebuyer considers taking a 30-year $300)000 mortgage, at the mortgage rate T12(m) = 6%. Sketch the pattern of scheduled principal

balance, scheduled interest, and principal payments. what will the monthly mortgage payments be?

(b) [8 marks] consider a MBS pass-through consisting of 100 identical

mortgages as in (a). That is, the principal of this pass-through is $30 million, the mortgage pool has a WAM = 360 months (30 years), and WAC = 6.0%. The pass-through security pays a coupon equal to

T12(P)T = 5%. ln the irst month, given the pSA level 200%, the monthly probability of prepayment is pt = 0.0334%. calculate the following

quantities for the irst month:

. Scheduled principal payment

. principal prepayment

. update of scheduled coupon payment for the following month . pass-through interest payment

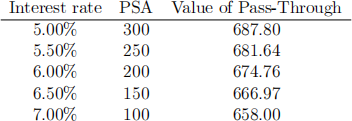

(c) [7 marks] The following table shows the impact of interest rates on the price of the pass-through. The current interest rate is 6%. calculate the efective duration and efective convexity of the pass-through.

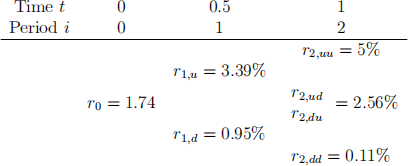

5. suppose the binomial tree of the 6-month continuously compounded interest rate is as follows:

The real-world probability p of an up movement is constant and equal to 1/2

along the tree. suppose that you observe the market prices of the following zero coupon bonds:

. P0 (i = 1) = 99.1338

. P0 (i = 2) = 97.8925

(a) [10 marks] Find:

. the market price of interest rate risk λ

. the risk neutral probability p*

. the price of a 1.5-year zero coupon bond P0 (i = 3), assuming the risk neutral probability is constant along the tree

(b) [8 marks] consider a straddle that at i = 2 (t = 1) pays the following amount:

payof at i = 2: V2 = max(P2 (3) - K, 0) 十 max(K - P2 (3), 0),

where K = 98.7282. Find the price of this security at time t = 0.

(c) [7 marks] Replicate the straddle deined in (b) using the bond expiring at i = 3 and the one period bond expiring at i + 1 along the tree. Find the position in both bonds at each node of the tree.

2023-07-31