ECO00056M Fixed Income Securities MSc Degree Examinations 2022-3

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECO00056M

MSc Degree Examinations 2022-3

Economics

Fixed Income Securities

Answer any THREE questions

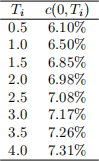

1. You observe the following swap rates c(0, Ti ) :

(a) Find the discount factors for each maturity. Do they imply any arbitrage opportunity in the market?

(b) Find the corresponding semiannually compounded interest rates r2 (, Ti ).

(c) What is the forward price for a 6% coupon bond with semiannual payments with delivery in 2 years and 2 year remaining maturity (at the delivery) Pc(fwd)(0, 2, 4)?

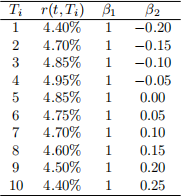

2. Consider T1 , T2 , ..., Tn to be points on the term structure of interest rates and let ri = r(t, Ti ) be the corresponding continuously compounded zero-coupon rates. You observe the following continuously compounded yield curve:

where β1 and β2 are the factor loadings in the interest rate model

dri = βi,1dφ 1 + βi,2dφ2 . (1)

(a) How (in terms of the term structure shape) can the factors φ1 and φ2 be interpreted? Find factor durations D1 and D2 for a 10−year 6% coupon bond with annual coupon payments.

(b) Suppose that you want to hedge your holding of the coupon bonds from (a) against changes in the two factors. Suppose that through the repo market you can at no cost take a position in a 1−year (Pz(S)) and 10−year (Pz(L)) zero-coupon bonds. Find the weights kS and kL in your hedging portfolio.

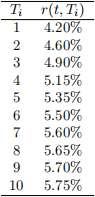

(c) Suppose that the next day, due to a central bank announcement, the interest rates are as follows:

How much has changed the value of the total portfolio that you found in (b)? How much would the value of the initial unhedged portfolio (i.e. the 10−year coupon bond from (a)) change without the hedge? Has the hedge worked?

3. A financial institution with total asset size of $2.6 million and asset dollar duration of $18.4 million has total liabilities of $1.6 million and dollar duration of $4.8 million. The duration of a 10−year coupon bond with the notional amount $100 paying 6% semiannually is 8.33.

(a) What position in the coupon bond should the bank assume to hedge the duration risk of its equity?

(b) Find duration and dollar duration of a fixed-for-floating (i.e. paying fixed) 10−year interest rate swap with 6% seminannual cash flows per $100 notional amount.

(c) If the financial institution wants to use the interest rate swap from (b) to hedge the interest rate risk of its equity, what should be the notional amount of the swap position?

4. Suppose that yields are normally distributed, such that

r(t + 1, T) ∼ N(Et [r(t + 1, T)],V art [r(t + 1, T)]), (2)

where the subscript ”t” means conditioning on information known at time t. At time t + 1, the price of a zero-coupon bond maturing at time T is

Pz (t + 1, T) = 100 × e −r(t+1,T) × (τ − 1) ,

where τ = T − t.

(a) Show that

log (Et [Pz (t + t, T)]) = Et [log(Pz (t + 1, T))] + ![]() (τ − 1)2 × V art [r(t + 1, T)]. (3)

(τ − 1)2 × V art [r(t + 1, T)]. (3)

Pz (t, T) = e− (r(t,t+1)+λt ) × Et [Pz (t + 1, T)]. (4)

Show that the expected log excess return on long period bond over one-period bond

Et llog( P![]() z(t)

z(t) ![]()

![]() ) )− log( Pz (t(0)

) )− log( Pz (t(0)![]() (5)

(5)

is equal to the log risk premium:

LRPt = λt − ![]() (τ − 1)2 × V art [r(t + 1, T)]. (6)

(τ − 1)2 × V art [r(t + 1, T)]. (6)

(c) Show that the slope of the term structure of interest rates is driven by both the expected changes in interest rates in the future and the log risk premium:

r(t, T) − r(t,t + 1) = (τ − 1)(Et [r(t + 1, T) − r(t, T)) + LRPt. (7)

5. You estimated the full Black, Derman and Toy (BDT) model and you found the following parameters (forward volatilities and continuously compounded interest rates in top nodes):

(a) Construct the whole BDT risk-neutral interest rate tree. Briefly explain the procedure.

(b) Find the value of the fixed-for-floating rate 3−year swap with the swap rate c = 3.4% on the notional amount $100 million. Recall that the swap cash flows are given by:

CF(Ti ) = ∆ × N × (r2 (Ti − ∆) − c).

(c) Find the value of the swaption on the swap defined in (b) with the swaption maturity 2 years from now (i.e. at T = 2).

2023-07-29