FINS3616 International Business Finance Term 3, 2022

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

FINS3616 International Business Finance

Term 3, 2022

Money Market Hedges of Receivables and Payables

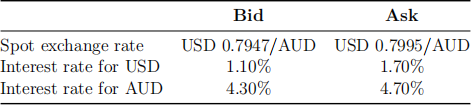

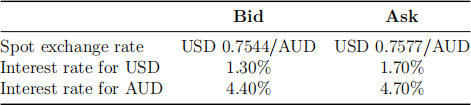

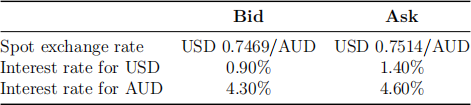

The following information is used for the next TWO questions.

You are the financial manager for K-Roo Ltd. and have received the below spot and interest rates quotes from AusBank:

Question 1

Assume that K-Roo Ltd. has a payable in AUD in one year and wishes to lock in an amount of USD that it will cost to cover this obligation. Rather than use AusBank’s forward ask rate, K-Roo instead wishes to again create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward ask price that K- Roo Ltd. is able to achieve to purchase the AUD needed to cover their obligation (by spending USD)?

Question 2

Suppose that K-Roo Ltd. has a receivable in AUD in one year’s time and wishes to lock in an amount of USD that it can be converted into. Rather than tap the forward markets directly by using AusBank’s forward bid rate, K- Roo instead wishes to create a portfolio using the using the spot and money market rates provided by the AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward bid price that K-Roo Ltd. is able to achieve for selling their AUD receivable to get USD?

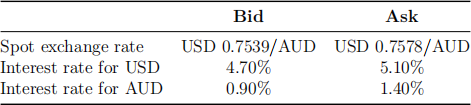

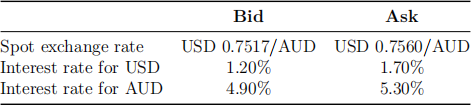

The following information is used for the next TWO questions.

You are the financial manager for K-Roo Ltd. and have received the below spot and interest rates quotes from AusBank:

Question 3

Suppose that K-Roo Ltd. has a receivable in AUD in one year’s time and wishes to lock in an amount of USD that it can be converted into. Rather than tap the forward markets directly by using AusBank’s forward bid rate, K- Roo instead wishes to create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward bid price that K-Roo Ltd. is able to achieve for selling their AUD receivable to get USD?

Question 4

Assume that K-Roo Ltd. has a payable in AUD in one year and wishes to lock in an amount of USD that it will cost to cover this obligation. Rather than use AusBank’s forward ask rate, K-Roo instead wishes to again create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward ask price that K- Roo is able to achieve to purchase the AUD needed to cover their obligation (by spending USD)?

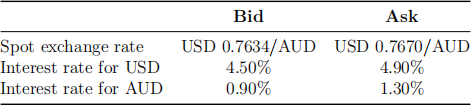

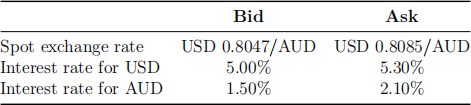

The following information is used for the next TWO questions.

You are the financial manager for K-Roo Ltd. and have received the below spot and interest rates quotes from AusBank:

Question 5

Assume that K-Roo Ltd. has a payable in AUD in one year and wishes to lock in an amount of USD that it will cost to cover this obligation. Rather than use AusBank’s forward ask rate, K-Roo instead wishes to again create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward ask price that K- Roo Ltd. is able to achieve to purchase the AUD needed to cover their obligation (by spending USD)?

Question 6

Suppose that K-Roo Ltd. has a receivable in AUD in one year’s time and wishes to lock in an amount of USD that it can be converted into. Rather than tap the forward markets directly by using AusBank’s forward bid rate, K- Roo instead wishes to create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward bid price that K-Roo Ltd. is able to achieve for selling their AUD receivable to get USD?

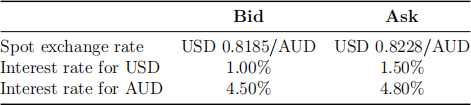

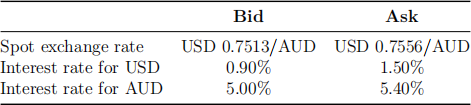

The following information is used for the next TWO questions.

You are the financial manager for K-Roo Ltd. and have received the below spot and interest rates quotes from AusBank:

Question 7

Suppose that K-Roo Ltd. has a receivable in AUD in one year’s time and wishes to lock in an amount of USD that it can be converted into. Rather than tap the forward markets directly by using AusBank’s forward bid rate, K- Roo instead wishes to create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward bid price that K-Roo Ltd. is able to achieve for selling their AUD receivable to get USD?

Question 8

Assume that K-Roo Ltd. has a payable in AUD in one year and wishes to lock in an amount of USD that it will cost to cover this obligation. Rather than use AusBank’s forward ask rate, K-Roo instead wishes to again create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward ask price that K- Roo Ltd. is able to achieve to purchase the AUD needed to cover their obligation (by spending USD)?

The following information is used for the next TWO questions.

You are the financial manager for K-Roo Ltd. and have received the below spot and interest rates quotes from AusBank:

Question 9

Assume that K-Roo Ltd. has a payable in AUD in one year and wishes to lock in an amount of USD that it will cost to cover this obligation. Rather than use AusBank’s forward ask rate, K-Roo instead wishes to again create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward ask price that K- Roo is able to achieve to purchase the AUD needed to cover their obligation (by spending USD)?

Question 10

Suppose that K-Roo Ltd. has a receivable in AUD in one year’s time and wishes to lock in an amount of USD that it can be converted into. Rather than tap the forward markets directly by using AusBank’s forward bid rate, K- Roo instead wishes to create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward bid price that K-Roo Ltd. is able to achieve for selling their AUD receivable to get USD?

The following information is used for the next TWO questions.

You are the financial manager for K-Roo Ltd. and have received the below spot and interest rates quotes from AusBank:

Question 11

Suppose that K-Roo Ltd. has a receivable in AUD in one year’s time and wishes to lock in an amount of USD that it can be converted into. Rather than tap the forward markets directly by using AusBank’s forward bid rate, K- Roo instead wishes to create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward bid price that K-Roo Ltd. is able to achieve for selling their AUD receivable to get USD?

Question 12

Assume that K-Roo Ltd. has a payable in AUD in one year and wishes to lock in an amount of USD that it will cost to cover this obligation. Rather than use AusBank’s forward ask rate, K-Roo instead wishes to again create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward ask price that K- Roo Ltd. is able to achieve to purchase the AUD needed to cover their obligation (by spending USD)?

The following information is used for the next TWO questions.

You are the financial manager for K-Roo Ltd. and have received the below spot and interest rates quotes from AusBank:

Question 13

Suppose that K-Roo Ltd. has a receivable in AUD in one year’s time and wishes to lock in an amount of USD that it can be converted into. Rather than tap the forward markets directly by using AusBank’s forward bid rate, K- Roo instead wishes to create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward bid price that K-Roo Ltd. is able to achieve for selling their AUD receivable to get USD?

Question 14

Assume that K-Roo Ltd. has a payable in AUD in one year and wishes to lock in an amount of USD that it will cost to cover this obligation. Rather than use AusBank’s forward ask rate, K-Roo instead wishes to again create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward ask price that K- Roo Ltd. is able to achieve to purchase the AUD needed to cover their obligation (by spending USD)?

The following information is used for the next TWO questions.

You are the financial manager for K-Roo Ltd. and have received the below spot and interest rates quotes from AusBank:

Question 15

Assume that K-Roo Ltd. has a payable in AUD in one year and wishes to lock in an amount of USD that it will cost to cover this obligation. Rather than use AusBank’s forward ask rate, K-Roo instead wishes to again create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward ask price that K- Roo Ltd. is able to achieve to purchase the AUD needed to cover their obligation (by spending USD)?

Question 16

Suppose that K-Roo Ltd. has a receivable in AUD in one year’s time and wishes to lock in an amount of USD that it can be converted into. Rather than tap the forward markets directly by using AusBank’s forward bid rate, K- Roo instead wishes to create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward bid price that K-Roo Ltd. is able to achieve for selling their AUD receivable to get USD?

The following information is used for the next TWO questions.

You are the financial manager for K-Roo Ltd. and have received the below spot and interest rates quotes from AusBank:

Question 17

Assume that K-Roo Ltd. has a payable in AUD in one year and wishes to lock in an amount of USD that it will cost to cover this obligation. Rather than use AusBank’s forward ask rate, K-Roo instead wishes to again create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward ask price that K- Roo Ltd. is able to achieve to purchase the AUD needed to cover their obligation (by spending USD)?

Question 18

Suppose that K-Roo Ltd. has a receivable in AUD in one year’s time and wishes to lock in an amount of USD that it can be converted into. Rather than tap the forward markets directly by using AusBank’s forward bid rate, K- Roo instead wishes to create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward bid price that K-Roo Ltd. is able to achieve for selling their AUD receivable to get USD?

The following information is used for the next TWO questions.

You are the financial manager for K-Roo Ltd. and have received the below spot and interest rates quotes from AusBank:

Question 19

Suppose that K-Roo Ltd. has a receivable in AUD in one year’s time and wishes to lock in an amount of USD that it can be converted into. Rather than tap the forward markets directly by using AusBank’s forward bid rate, K- Roo instead wishes to create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward bid price that K-Roo Ltd. is able to achieve for selling their AUD receivable to get USD?

Question 20

Assume that K-Roo Ltd. has a payable in AUD in one year and wishes to lock in an amount of USD that it will cost to cover this obligation. Rather than use AusBank’s forward ask rate, K-Roo instead wishes to again create a portfolio using the using the spot and money market rates provided by AusBank to achieve the same thing.

According to CIRP, what is the effective one year forward ask price that K- Roo Ltd. is able to achieve to purchase the AUD needed to cover their obligation (by spending USD)?

2023-07-25

Money Market Hedges of Receivables and Payables