FINM7405 Finance Semester One Examinations, 2022

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Semester One Examinations, 2022

FINM7405 Finance

Question 1

The price of a European put that expires in 6 months and has a strike price of $10 is $2. The underlying stock price is currently valued at $9, and risk-free rate is 2% p.a.

a) What is the price of a European call with the same strike price and maturity as the put?

b) Suppose that the European call is currently priced at $1.20. Devise a strategy to arbitrage from this situation. What is the net payoff of your arbitrage strategy at t=0 and at t=T (i.e. at the maturity of the options)? Explain what happen at t=T.

c) Ignore part (b). Suppose that the European call is currently priced at $1.00. Devise a strategy to arbitrage from this situation. What is the net payoff of your arbitrage strategy

Question 2

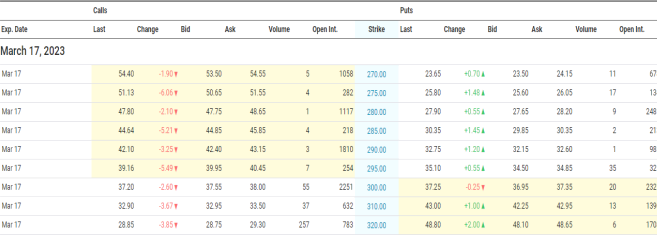

Consider the following information on the options available on stock Netflix. You intend to buy one March maturity call option on company Netflix’s stock with exercise price $280 and buy one March maturity put option on the same underlying asset with strike price $300. The information of the options on the stock of the company is as follows (use last price as the price of the options):

a. Graph the payoff and profit/loss of this portfolio at option expiration.

b. What will be the profit/loss on this portfolio if company Netflix trades at $290 on the option maturity date?

c. Given the portfolio that you have constructed, what is most likely your view of the future for the price of Netflix’s stock?

Question 3

An Australia company has just issued a 3-year EuroPound bond in SGD dollar which is priced on par at SGD 100. As an experienced manager, you are required to hedge the position of your company using a

‘fixed-for-fixed’ currency swap. You observe the following current information:

• Spot foreign exchange rate = AUD0.99 for 1 SGD

• The tenor of the swap is 3 years

• Interest is repaid every half a year

• The inferred market yield of an equivalent 3-year AUD bond is 4% pa

• The inferred market yield of an equivalent 3-year SGD bond is 6% pa

a. With respect to the currency swap, how much are you lending and borrowing and in what currency for each?

b) Three months have passed. The swap now has 33 months to maturity. The market yield of an equivalent 33-months to maturity AUD bond is 4.5% pa. The market yield of an equivalent 33-months to maturity SGD bond is 5% pa. Today’s spot exchange rate is AUD0.96 for 1 SGD. If you and the swap counterparty decided to terminate the swap today via ‘mutual agreement’, how much do you have to pay or receive to settle the swap termination?

c) Now, 2 years have passed since the initiation of the swap and the swap now has 1 year to maturity. The market yield of an equivalent 1-year AUD bond remains at 4% pa. Likewise, the market yield of an equivalent 1-year SGD bond remains at 6% pa. What is the value of the swap to you if the current spot exchange rate remains at AUD$0.99 = SGD$1? If the current spot exchange rate changes to

AUD$0.8 = SGD$1? If the current spot exchange rate decreases to AUD$1.1=SGD$1?

2023-06-02