FINM7407 –Financial Institutions and Markets Semester 1 2023

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

FINM7407 –Financial Institutions and Markets

Semester 1 2023 Sample Final Examination Solution

This exam has 55 marks in total and carries 55% of the total mark of this course. There are eight (8) questions.

Answer all questions.

Question 1 [8 marks]

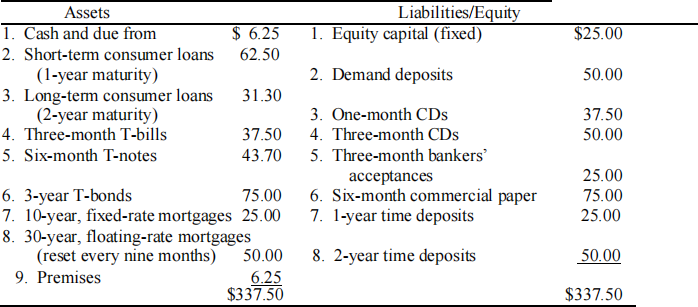

Consider the following balance sheet for MMC Bancorp (in millions of dollars):

a. Calculate the value of MMC’s rate-sensitive assets, rate sensitive liabilities, and cumulative gap over the next year. What does the gap suggest?

Looking down the asset side of the balance sheet, we see the following one-year rate-sensitive assets (RSA):

1. Short-term consumer loans: $62.50 million, which are repriced at the end of the year and just make the one-year cutoff.

2. Three-month T-bills: $37.50 million, which are repriced on maturity (rollover) every three months.

3. Six-month T-notes: $43.70 million, which are repriced on maturity (rollover) every six months.

4. 30-year floating-rate mortgages: $50.00 million, which are repriced (i.e., the mortgage rate is reset) every nine months. Thus, these long-term assets are RSA in the context of the repricing model with a one-year repricing horizon.

Summing these four items produces one-year RSA of $193.70 million. The remaining $143.80 million is not rate sensitive over the one-year repricing horizon. A change in the level of interest rates will not affect the interest revenue generated by these assets over the next year. The $6.25 million in the cash and due from category and the $6.25 million in premises are nonearning assets. Although the $131.30 million in long-term consumer loans, 3-year Treasury bonds, and 10-year, fixed-rate mortgages generate interest revenue, the level of revenue generated will not change over the next year since the interest rates on these assets are not expected to change (i.e., they are fixed over the next year).

Looking down the liability side of the balance sheet, we see that the following liability items clearly fit the one-year rate or repricing sensitivity test:

1. One-month CDs: $37.50 million, which mature in one months and are repriced on rollover.

2. Three-month CDs: $50 million, which mature in three months and are repriced on rollover.

3. Three-month bankers’ acceptances: $25 million, which mature in three months and are repriced on rollover.

4. Six-month commercial paper: $75 million, which mature and are repriced every six months.

5. 1-year time deposits: $25 million, which are repriced at the end of the one-year gap horizon.

Summing these five items produces one-year rate-sensitive liabilities (RSL) of $212.5 million. The remaining $125 million is not rate sensitive over the one-year period. The $25 million in equity capital and $50 million in demand deposits do not pay interest and are therefore classified as nonpaying. The $50 million in two-year time deposits generate interest expense over the next year, but the level of the interest generated will not change if the general level of interest rates change. Thus, we classify these items asfixed-rate liabilities.

The five repriced liabilities ($37.50 + $50 + $25 + $75 + $25) sum to $212.5 million, and the four repriced assets of $62.50 + $37.50 + $43.70 + $50 sum to $193.70 million. Given this, the cumulative one-year repricing gap (CGAP) for the bank is:

CGAP = (One-year RSA) - (One-year RSL) = RSA - RSL = $193.70 million - $212.5 million = - $18.80 million

The CGAP suggests a negative relation between the change in interest rates and the change in the FI’s NII.

b. If interest rates rise by 1 percent on both RSAs and RSLs, calculate the expected change in the net interest income for the FI

The CGAP effect suggests a reduction in reduction in net interest income of the FI when interest rates increase

![]() NII = CGAP x

NII = CGAP x ![]() R (=

R (=![]() RRSA=

RRSA=![]() RRSL)

RRSL)

= (-$18.80 million) x 0.01

= -$188,000

c. If interest rates rise by 1.2 percent on RSAs and by 1 percent on RSLs, calculate the change in the spread and what does the spread suggest?

![]() S =

S = ![]() RRSA -

RRSA - ![]() RRSL = 0.012-0.01=0.002

RRSL = 0.012-0.01=0.002

The spread effects suggests that there is a positive relation between the change in interest rates and the change in NII. In other words, the spread effect suggests an increase in NII when interest rates increase.

d. Calculate the expected change in the net interest income for the FI.

![]() NII = [RSA x

NII = [RSA x ![]() RRSA] - [RSL x

RRSA] - [RSL x ![]() RRSL]

RRSL]

= [$193.70 million x 1.2%] - [$212.5 million x 1.0%]

= $2.3244 million - $2.125 million

= $199,400

e. Explain how the CGAP and spread effects influence the change in net interest income.

When interest rates increase, the expected change in NII comes from combining the spread effect (an increase in NII) and the CGAP effect (a reduction in NII)

![]() NII = [RSA x

NII = [RSA x ![]() RRSA] - [RSL x

RRSA] - [RSL x ![]() RRSL]

RRSL]

![]() NII = RSA x [

NII = RSA x [![]() S +

S + ![]() RRSL] - [RSL x

RRSL] - [RSL x ![]() RRSL]

RRSL]

![]() NII = RSA x

NII = RSA x ![]() S + [RSA – RSL] x

S + [RSA – RSL] x ![]() RRSL

RRSL

![]() NII = RSA x

NII = RSA x ![]() S + CGAPx

S + CGAPx![]() RRSL

RRSL

= 193.70 x 0.002 + (- 18.8) x 0.01 = 0.3874 – 0.1880 = 0.1994 = $199,400

In this case, the increase in NII because an increase in NII due to the spread effect dominates the decrease in NII due to the CGAP effect.

Question 2 [4 marks]

A bank is planning to make a loan of $5,000,000 to a firm in the steel industry. It expects to charge a servicing fee of 50 basis points. The loan has a maturity of 8 years with a duration of 7.5 years. The cost of funds (the RAROC benchmark) for the bank is 10 percent. The bank has estimated the maximum change in the risk premium on the steel manufacturing sector to be approximately 4.2 percent, based on two years of historical data. The current market interest rate for loans in this sector is 12 percent.

a. Using the RAROC model, determine whether the bank should make the loan? RAROC = Fees and interest earned on loan/Loan or capital risk

Loan risk, or ![]() LN = -DLN x LN x (

LN = -DLN x LN x (![]() R/(1 + R)) = -7.5 x $5m x (0.042/1. 12) = -$1,406,250

R/(1 + R)) = -7.5 x $5m x (0.042/1. 12) = -$1,406,250

Expected interest = 0.12 x $5,000,000 = $600,000

Servicing fees = 0.0050 x $5,000,000 = $25,000

Less cost of funds = 0.10 x $5,000,000 = -$500,000

Net interest and fee income = $125,000

RAROC = $125,000/1,406,250 = 8.89 percent. Since RAROC is lower than the cost of funds to the bank, the bank should not make the loan.

b. What should be the duration in order for this loan to be approved?

For RAROC to be 10 percent, loan risk should be:

$125,000/![]() LN= 0.10

LN= 0.10 ![]()

![]() LN= 125,000 / 0.10 = $1,250,000

LN= 125,000 / 0.10 = $1,250,000

![]() -DLN x LN x (

-DLN x LN x (![]() R/(1 + R)) = 1,250,000

R/(1 + R)) = 1,250,000

DLN = 1,250,000/(5,000,000 x (0.042/1. 12)) = 6.67 years.

Thus, this loan can be made if the duration is reduced to 6.67 years from 7.5 years.

c. Assuming that duration cannot be changed, how much additional interest and fee income will be necessary to make the loan acceptable?

Necessary RAROC = Income/Risk ![]() Income = RAROC x Risk

Income = RAROC x Risk

= $1,406,250 x 0.10 = $140,625

Therefore, additional income = $140,625 - $125,000 = $15,625, or

$15,625/$5,000,000 = 0.003125 = 0.3125%.

Thus, this loan can be made if fees are increased from 50 basis points to 81.25 basis points.

d. Given the proposed income stream and the negotiated duration, what adjustment in the loan rate would be necessary to make the loan acceptable?

Need an additional $15,625 => $15,625/$5,000,000 = 0.003125 or 0.3125%

Expected interest = 0.123125 x $5,000,000 = $615,625

Servicing fees = 0.0050 x $5,000,000 = $25,000

Less cost of funds = 0.10 x $5,000,000 = -$500,000

Net interest and fee income = $140,625

RAROC = $140,625/1,406,250 = 10.00 percent = cost of funds to the bank. Thus, increasing the loan rate from 12% to 12.3125% will make the loan acceptable

Question 3 [6 marks]

Consider $100 million of 30-year mortgages with a coupon of 5 percent per year paid quarterly.

a. What is the quarterly mortgage payment?

There are 120 quarterly payments over 30 years. The quarterly mortgage payments are $100m = PVAn=120, k=1.25% x PMT => PMT = $1,613,350.

b. What are the interest and principal repayments over the first year of life of the mortgages?

(Fixed) Interest Principal Remaining

Quarter Balance Payment Payment Payment Principal

1 $100,000,000 $1,613,350 $1,250,000 $363,350 $99,636,650

2 99,636,650 1,613,350 1,245,458 367,891 99,268,759

3 99,268,759 1,613,350 1,240,859 372,490 98,896,269

4 98,896,269 1,613,350 1,236,203 377,146 98,519,123

c. Construct a 30-year CMO using this mortgage pool as collateral. The pool has three tranches, where tranche A offers the least protection against prepayment and tranche C offers the most protection against prepayment. Tranche A of $25 million receives quarterly payments at 4 percent per year, tranche B of $50 million receives quarterly payments at 5 percent per year, and tranche C of $25 million receives quarterly payments at 6 percent per year.

Principal amount Interest rate Quarterly interest on

initial balance Quarterly amortization

Tranche A

$25 million

4 percent

$250,000

Tranche B

$50 million

5 percent

$625,000

Tranche C

$25 million

6 percent

$375,000

Total Issue $100 million 5 percent

$1,250,000

$1,613,350

d. Assume nonamortization of principal and no prepayments. What are the total promised coupon payments to the three classes? What are the principal payments to each of the three classes for the first year?

Regular tranche A interest payments are $250,000 quarterly. If there are no prepayments, then the regular GNMA quarterly payment of $1,613,350 is distributed among the three tranches. Five million is the total coupon interest payment for all three tranches. Therefore, $363,350 of principal is repaid each quarter. Tranche A receives all principal payments. Tranche A cash flows are $250,000 + $363,350 = $613,350 quarterly. The cash flows to tranches B and C are the scheduled interest payments.

Tranche A amortization schedule

|

Fixed Interest Principal Remaining Quarter Balance Payment Payment Payment Principal |

|||||

|

1 |

25,000,000 |

613,350 |

250,000 |

363,350 |

24,636,650 |

|

2 |

24,636,650 |

613,350 |

246,367 |

366,983 |

24,269,667 |

|

3 |

24,269,667 |

613,350 |

242,697 |

370,653 |

23,899,014 |

|

4 |

23,899,014 |

613,350 |

238,990 |

374,359 |

23,524,655 |

Tranche B amortization schedule

|

|

|

Fixed |

Interest |

Principal |

Remaining |

|

Quarter |

Balance |

Payment |

Payment |

Payment |

Principal |

|

1 |

50,000,000 |

625,000 |

625,000 |

0 |

50,000,000 |

|

2 |

50,000,000 |

625,000 |

625,000 |

0 |

50,000,000 |

|

3 |

50,000,000 |

625,000 |

625,000 |

0 |

50,000,000 |

|

4 |

50,000,000 |

625,000 |

625,000 |

0 |

50,000,000 |

Tranche C amortization schedule

|

|

|

Fixed |

Interest |

Principal |

Remaining |

|

Quarter |

Balance |

Payment |

Payment |

Payment |

Principal |

|

1 |

25,000,000 |

375,000 |

375,000 |

0 |

25,000,000 |

|

2 |

25,000,000 |

375,000 |

375,000 |

0 |

25,000,000 |

|

3 |

25,000,000 |

375,000 |

375,000 |

0 |

25,000,000 |

|

4 |

25,000,000 |

375,000 |

375,000 |

0 |

25,000,000 |

e. If, over the first year, the trustee receives quarterly prepayments of $5 million on the mortgage pool, how are these funds distributed?

The quarterly prepayments of $5 million will be credited entirely to tranche A until tranche A is completely retired. Then prepayments will be paid entirely to tranche B. The amortization schedule for tranche A for the first year is shown below. This amortization schedule assumes that the trustee has a quarterly payment amount from the mortgage pool of $1,613,350.

2023-05-29