ECMT3150: Mid-Semester Test (2021s1)

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

ECMT3150: Mid-Semester Test (2021s1)

Time allowed: 1.5 hours

21 April 2021

The total score of this exam is 60 marks. Attempt all the four questions.

1. (Total: 13 marks) Conceptual questions:

(a) (4 marks) What is a random walk? Give an example.

(b) (4 marks) Explain the key di§erence between spurious regression and cointegration.

(c) (5 marks) ìIt is impossible to predict a white noise process,îBob said. Do you agree with Bob? Explain your answer with an example.

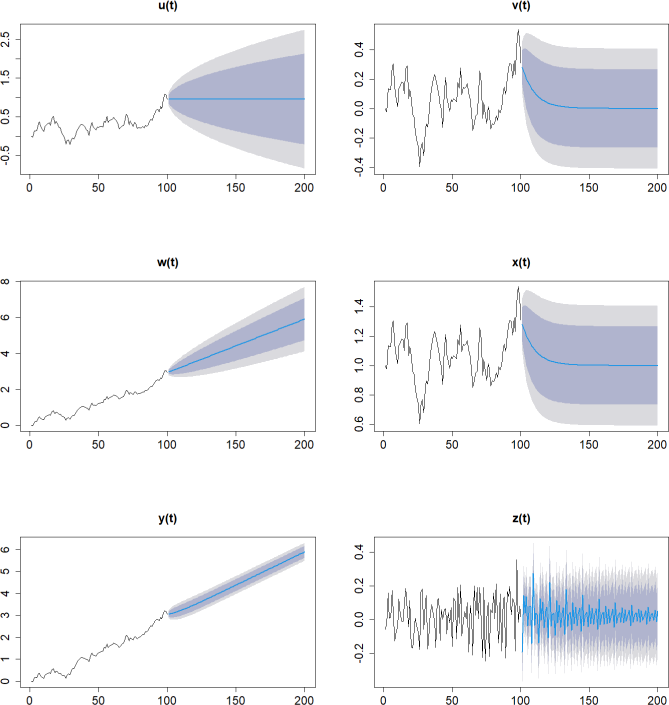

2. (Total: 12 marks) The plots show the sample trajectory and the forecast (both the point forecast and the conÖdence intervals) generated by di§erent time series models. From the following list, pick one DGP that you believe will generate the sample path and forecast as displayed in each plot.

(a) rt = 0:9rt — 1 + et .

(b) rt = 0:9rt — 12 + et .

(c) rt = 0:9rt —4 + et .

(d) rt = 0:1 + 0:9rt — 1 + et .

(e) rt = 1 + 0:9rt — 1 + et .

(f) rt = 0:003t + 0:9rt — 1 + et .

(g) rt = rt — 1 + et .

(h) rt = 0:005 + rt — 1 + et .

(i) rt = 0:005 + 0:0032t + rt — 1 + et .

3. (Total: 15 marks) Let Jt be the indicator that a jump occurs in the stock market. The joint probability distribution of Jt — 1 and Jt is given in the table below, where p11 , p10 , p01 and p00 are constants. The row and column sums are displayed to the right and below the double lines, respectively.

|

|

Jt = 1 Jt = 0 |

|

||

|

Jt — 1 = 1 Jt — 1 = 0 |

p11 p01 |

p10 p00 |

|

0.1 0.9 |

|

|

0.2 0.8 |

|

|

|

3. (a) (2 marks) Find E(Jt) and Var(Jt).

(b) (2 marks) Is the process {Jt} stationary? Explain.

(c) (3 marks) Find the conditional distribution of Jt given that a jump occurs at time t _ 1. Express your answer in terms of p11 .

(d) (3 marks) Find the conditional variance of Jt given that a jump occurs at time t _ 1. Express your answer in terms of p11 .

(e) (2 marks) Suppose the jump occurrences are independent. Find the value of p00 .

(f) (3 marks) Suppose the jump occurrences are positively correlated. Find the range of

values of p00 .

4. (Total: 20 marks) Mimi, an ECMT3150 student, studies the following AR(2) process

yt = 0:1 + 0:9yt —2 + "t ,

where "t ~ iid N(0; 0:25) (normal distribution with mean 0 and variance 0:25).

(a) (3 marks) Find the unconditional mean and variance of yt .

(b) (4 marks) Derive the autocorrelation function (ACF) of yt as a function of lag. Plot

the ACF against lag.

(c) (1 mark) Plot the partial autocorrelation function (PACF) of yt against lag.

(d) (3 marks) Express the given AR(2) process as an MA(o) process. Describe how a shock at time 1 impacts the subsequent values of yt .

(e) Suppose Mimi is currently standing at time T and observes the latest realised values of the time series to be yT — 1 = 1:2 and yT = 0:8. Let yT (`) be the optimal `-step ahead forecast obtained as at time T.

i. (3 marks) Derive the point forecast yT (10).

ii. (3 marks) Derive the 95% conÖdence interval for yT (10).

iii. (3 marks) What are the limits of yT (`) and s:d:(yT (`)) as ` 二 o?

2023-04-06