Data Science & Machine Learning in Finance (ACCFIN5246)

Hello, dear friend, you can consult us at any time if you have any questions, add WeChat: daixieit

Data Science & Machine Learning in Finance (ACCFIN5246)

Group Assignment – Spring 2023

Deadline: 3 March, noon

This assignment counts towards 25% of the overall course grade.

Instruction

— Answer all questions.

— This is a group assessment.

— Submission to be made electronically via the course Moodle page. This includes a written

report including analytical steps taken, numerical answers, diagrams, tables and comments. Please submit only the main report (no additional spreadsheet, software routine, etc. is required), however you can include additional tables or developed routines as appendixes (clearly explain the reason to include any additional appendix).

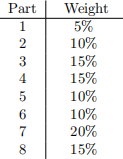

— Clearly number each part. Each part in the assignment carries a weight described below:

— You can use a calculator or a software to carry out computations.

— Results should be reported in a clear format. Avoid reporting numbers in ‘scientific format’

e.g. 7 .2031e-06. All reported numbers should be rounded to two decimal points. For example, report 0.00 in place of 7 .2031e-06.

THE MopEL Consider the capital asset pricing model characterised by the following specification denoted as Model(A) used to interrelate the real excess return, on a given asset rt − rf,t where rf,t is the risk-free rate, to the market real return denoted by rm,t :

(1)

(1)

note that the object of interest is the time-varying feature of the coefficients ![]() w and

w and ![]() w . In particular,

w . In particular, ![]() w summarizes the conditional relationship, given a rolling window incorporating a consecutive but limited span of data, between the market risk premium rM,t − rf,t and the excess return.

w summarizes the conditional relationship, given a rolling window incorporating a consecutive but limited span of data, between the market risk premium rM,t − rf,t and the excess return.

DATA You are required to obtain data for the variables needed to construct and estimate the model, in particular,

❼ The data covers the period 2000/01/03-2022/03/31, on a daily basis.

❼ (rt ) real returns, associated MSFT stock, acquired from the Wharton Research platform (WRDS): https://wrds-www.wharton.upenn.edu/.

❼ (rM,t ) real returns, associated with US equity market described by the

S&P500 composite market index. You can use either the price or return data according to your setting (i.e. locally transform prices to returns).

❼ (rf,t ) real returns, associated with US treasuries (10-years maturities) — this can be acquired from WRDS or FRED (https://fred.stlouisfed. org/).

❼ You can use the US consumer price index to transform nominal data

into real terms. This data can be acquired from several sources, includ- ing the Federal Reserve Economic Data (FRED) at (https://fred. stlouisfed.org/).

Based on the data you acquire and the specification above and complete parts [1]- [8]:

Part [1] Construct real excess MSFT log-returns (zr) and real excess market log-![]() returns (zrm). Clearly report only the precise values for two averages: zr and zrm over the entire sample in net returns and based on the original daily frequency (rounded to two decimal points e.g. 12.34%). (Mark: 5%)

returns (zrm). Clearly report only the precise values for two averages: zr and zrm over the entire sample in net returns and based on the original daily frequency (rounded to two decimal points e.g. 12.34%). (Mark: 5%)

Implement a code to estimate specification (1), as a rolling window where w = 25. This indicates that windows include 25 consecutive days and rolling forward by one day, amounts to a new window (each two neighbouring windows overlap for 24 days). Store all values obtained for ![]() w and

w and ![]() w .

w .

Part [2] Restrict the results (remove values outside the intervals only for the purpose of this part) to −2% ≤ ![]() w ≤ 2% and

w ≤ 2% and ![]() w ≥ −1. Evaluate the following specification,

w ≥ −1. Evaluate the following specification, ![]() w = 90 + 91

w = 90 + 91 ![]() w + ei . Report the precise value for

w + ei . Report the precise value for ![]() 1 and its p-value (rounded to two decimal points). (Mark: 10%)

1 and its p-value (rounded to two decimal points). (Mark: 10%)

Part [3] Briefly comment on the results obtained in Part [2]. The comments should relate the statistical finding to the financial interpretations (Con- cise and less than 200 words). (Mark: 15%)

Develop a formal constrained least squares (CLS) framework to impose all constraints characterised in Part [2] to the estimation.

Part [4] Define the constraints RΘ ≤ r where Θ = [90 , 91]\ and that R and r are defined according to the baseline CLS definition. Write down the exact setup values used to characterise the constrained problem used for R and r and also the formal hypothesis testing in terms of the H0 and the alternative. (Mark: 15%)

Part [5] Report the exact value for RssC − RssU . (Mark: 10%)

Part [6] What is the test statistic? What is the critical value? (Mark: 10%)

For the following two parts, you will need to conduct further research on MSFT and market returns trends.

Part [7] What is the most prominent underlying economic or financial driver, in this context, leading to rejecting the null hypothesis? Only mention one factor and explain how this factor is directly linked to the test outcome (200 words). (Mark: 20%)

Part [8] Propose an alternative specification in place of equation (1) to incorporate the factor you highlighted in Part [7]. This should be a specification, with all terms defined and explained. Provide concise comments. (Mark: 15%)

2023-03-18